|

1.The Firm

A technical

unit engaged in the production of one or a group of related commodities. In

theory, perceived as a single product firm with the entrepreneur serving as a

surrogate for a decision-making hierarchy and involving the study mainly of

external behavior and only ‘cost analysis’ of production decisions,

i.e. not business management.

2. Production

Creation of goods and/or services, which, directly or indirectly, satisfy human

wants, needs and desires. Through production the firm

puts utility into such goods & services generating supply which is the obverse of consumer demand

which involves the extraction of utility.

In theory, production is viewed as the only function of the firm.

Through supplying commodities demanded by consumers, the firm strives to maximize

profits.

3. Input/Factors of Production

Any good or service which

contributes to the production of output. Factors include:

capital (K; labour (L); natural resources (N); and entrepreneurship. This last factor

is poorly defined and resists empirical measurement. For those

interested in a fuller description of these factors of production,

please see

Observation #6: Capital. Labour & Natural Resources.

4. Cost

(MKM

C13/276; 257-259;

282-284;

262-264)

Cost is the price of factors of production used in producing output. Along with

Price

and Quantity of final output, Cost is a key economic decision-making factor.

5. Output

Output is the result of transforming inputs into goods or services which satisfy,

directly or indirectly, human wants, needs and desires. Output

increases until the additional or marginal revenue earned for the last unit sold

equals its marginal cost.

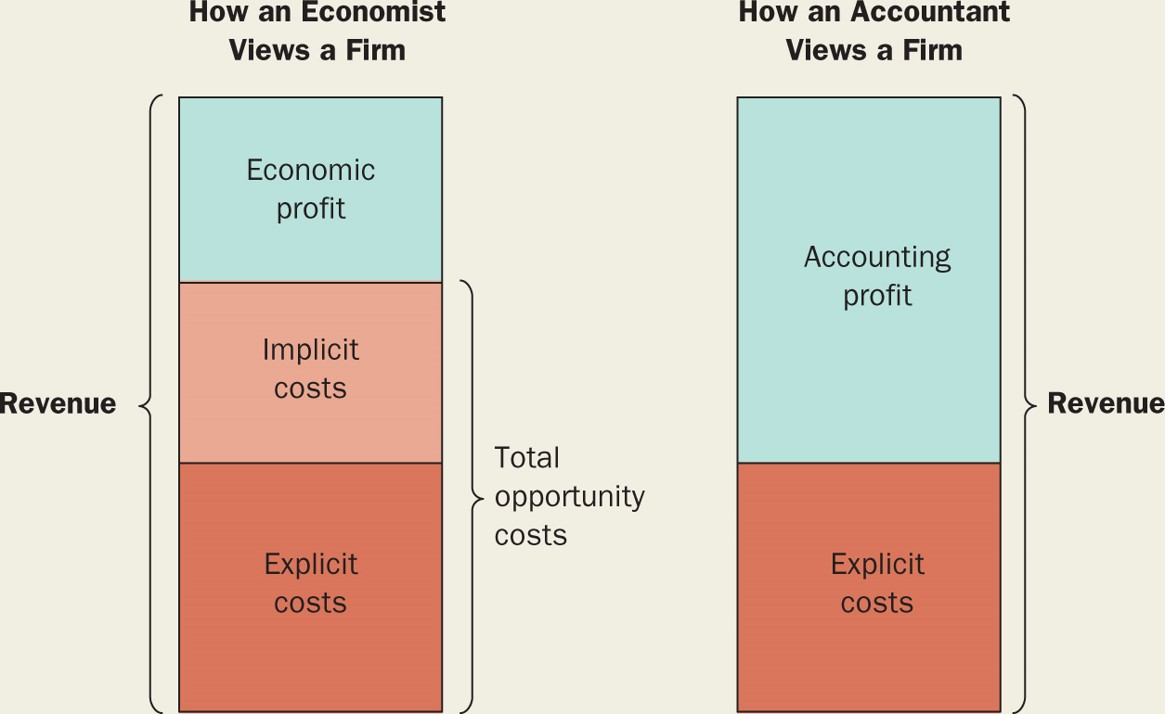

6. Profits

(MKM

C13/276; 258-259;

284-285;

264)

Profit is the residual

of Revenue (Price times

Quantity sold)

earned by the entrepreneur after all other factors of production have been

paid. It is

compensation for uncertainty and entrepreneurship ideally earning normal profits

(the opportunity costs of entrepreneurship) but sometimes earning monopoly, excess

or economic profits. In theory,

profit is the raison d’etre of the firm which can be gained, however, only by

satisfying consumer wants, needs and desires.

The distinction

between 'normal' profits

- the opportunity cost of entrepreneurship - and 'economic' profits,

i.e., in excess of normal profits, need be remembered.

There are thus 'good' and 'bad' profits in Economics

(MKM

Figure 13.1).

7. Ownership

vs.

Control

A firm may be owned and controlled by the same individual or group, or these two

functions may be separated. In

theory, it is assumed there is no significant effect of their separation and

profit maximization remains the functional objective of the firm.

8. Diversification

The distribution of productive investment across geographic space, or

multiplying the number and types of outputs in order to insure profit stability

by offsetting gains and losses. Geographic diversification is not formally considered except as

additions to factor cost. Similarly

multiple outputs not considered in the Standard Model.

|

{kind=link}