|

5.1 Fiscal Policy:

Tax & Spend (MKM C15/391-413:

366-87;

C16/ 384-403;

361-379)

While the Great

Depression of the 1930s was the most severe and long lasting, it was but a

single link a long chain of business cycle boom/busts dating back to the

beginning of the Industrial Revolution. Until the Keynesian Revolution of

1936 Government played little if any role in managing the national economy.

Rather the business cycle was allowed to run its course according to the 'iron

law of wages'. In the boom, labour becames scarce and wages rose. In

the bust, labour was increasingly unemployed. Wages fell until low enough

for firms to re-hire beginning the upswing of the business cycle. Meanwhile

workers became increasingly desperate in the downturn. There was no social

safety net like unemployment insurance, welfare or medicare.

The

Keynesian Revolution established that Government should spend in bad and save in

good days. It also dictated Government's reaction to the business cycle should

be both automatic as well as discretionary. In this new architecture of public

finance, automatic stabilizers are triggered by 'objective' changes in the

economy and implemented automatically according to an existing Act of

Parliament, e.g., if unemployment rises, employment insurance payments increase. Discretionary fiscal policy action, on the other hand, requires debate in

Parliament of proposed legislation to mandate a new fiscal policy initiative,

e.g., changes in the income tax rate or increases in defense or other public

spending. Such discretionary action is justified if and only if automatic

stabilizers fail or are thought to fail to moderate the business cycle. This

'moderating the business cycle' is called 'counter-cyclical fiscal policy'.

If

the boom rises to fast, slow it down; if the bust falls too fast, slow it down.

A primary goal of fiscal policy, in the Keynesian sense, is to moderate the business cycle, to stabilize the economy. And linked to

moderating the business cycle is to do so while, at the same time, fostering growth

in potential GDP.

Keynes provided a tool to allow Government to stabilize the business cycle

without having to do it all itself. It is 'the multiplier'. He also spawned a

generation of economists who searched for new tools to foster growth in

potential GDP, i.e., how to make the economy grow. Growth theory is now a

recognized sub-discipline of the economics profession. The alleged failure of Keynesian economics between the 1960s and

1990s in fact represented Government choosing to spend on the upside as well as

the downside of the business cycle. This partially reflected 'policy lags',

i.e., recognize a problem, fashion a solution, implement it and wait for

the desired results. In other words, the impact of some Government

programs were simply out of phase with the business cycle. However, the

'guns & butter' policy of the American Government during the Vietnam War,

i.e., no special taxes were levied to pay for the war, meant Government

borrowed on the financial markets and increased the national debt. A

similar guns & butter policy also characterized the second 2003 Gulf War.

Arguably, it was not Keynesian policy but politics that failed.

For those interested in the political actors involved in fiscal

policy, please see:

Observation #5: Economics of Democracy.

For those interested the budgetary process, please see:

Observation #6: Fiscal Policy in Canada.

i - Assets,

Liabilities, Revenue & Expenditures

CSGFMS

ASSETS & LIABILITIES

|

Assets

|

Liabilities

|

|

1.

Cash on Hand & Deposits

|

1.

Borrowings from Financial Institutions

|

|

2.

Receivables

|

2.

Payables

|

|

3.

Loans & Advances to

|

3.

Loans & Advances from

|

|

4.

Investments

|

4.

Savings Bonds, Treasury Bills & Other Short-Term

|

|

5.

Other Financial Assets

|

5.

Bonds, Debentures & Treasury Bills – Long-Term

|

|

|

6.

Pension Plans, Deposit & Other Liabilities

|

|

|

Excess of

Financial Assets over Liabilities |

|

|

|

REVENUE

|

Taxes |

|

|

1.

Personal Income Taxes

|

14.

Succession Duties & Estate Taxes

|

|

2.

Payroll Taxes

|

15.

Gift Taxes

|

|

3.

Corporation Income Tax

|

16.

Health Insurance Premiums

|

|

4.

Taxes on Insurance Premiums

|

17.

Social Insurance Levies

|

|

5.

Other Taxes on Corporations & Businesses

|

18.

Universal Pension Plan Levies

|

|

6.

Taxes on Certain Payments & Credits to Non-Residents

|

19.

Other Taxes

|

|

7.

Real & Personal Property Taxes

|

Non-Taxes |

|

8.

General Sales Taxes

|

20.

Natural Resource Revenues

|

|

9.

Motor Fuel Taxes

|

21.

Privileges, Licences & Permits

|

|

10. Alcoholic

Beverages Taxes

|

22.Sales of

Goods & Services

|

|

11.

Tobacco Taxes

|

23.

Return on Investments

|

|

12.

Taxes on Amusements & Admissions

|

24.

Other Revenues from Own Sources

|

|

13.

Taxes on Other Commodities & Services

|

25.

Miscellaneous

|

EXPENDITURE

|

1.

General Government

|

11.

Labour, Employment & Immigration

|

|

2.

Protection of Persons & Property

|

12.

Housing

|

|

3. Transportation & Communications

|

13. Foreign Affairs & International Assistance

|

|

4. Health

|

14. Supervision and Development of Regions &

Localities

|

|

5. Social Welfare

|

15. Research Establishments

|

|

6. Education

|

16. General Purpose Transfers to Other Levels of

Government

|

|

7. Environment

|

17. Transfers to Own Enterprises

|

|

8. Natural Resources

|

18. Debt Charges

|

|

9. Agriculture, Trade and Industry, and Tourism

|

19. Other

|

|

10. Recreation & Culture

|

|

ii -Fiscal Policy Multipliers

But

how can discretionary fiscal policy

lever change the macroeconomy - assuming potential GDP is fixed.

After the budget debate about how much pleasure and pain, the composite total

(not allowing for 'distributional' effects) of tax and spend results in an

increase, a decrease or no change in autonomous aggregate expenditure. An

increase or decrease will change aggregate expenditure more than the initial

change via three fiscal policy multipliers assuming the short-run and

a constant price level. These are:

a) Autonomous/Government Expenditure Multiplier

b) Autonomous Tax Multiplier

c) Balanced Budget Multiplier

d) Impact of the Marginal Propensity to Import (MPM)

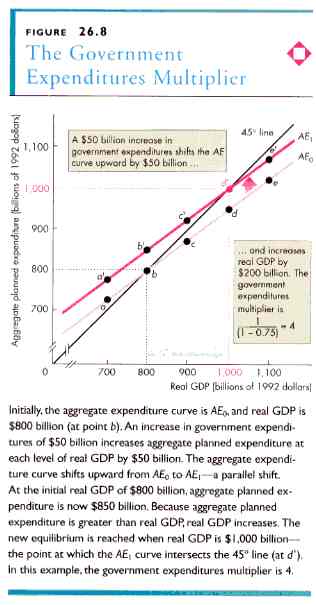

a) Autonomous/Government Expenditure Multiplier (GEM)

The GEM depends on the marginal

propensity to consumer (P&B 4th Ed

Fig. 26.8;

MKM Fig. 15.8). The higher MPC, i.e., the steeper the slope of the aggregate expenditure curve (AEC), the

greater GEM. The lower MPC, the gentler the slope of the AEC, the lower

GEM. MPC, however, is assumed to be constant. GEM = 1/1-b =

∆Y/∆G.

Say the MPC is .75 then Gem is 1/1-.75 = 1/.25 = 4. The same multiplier

applies to any autonomous expenditure change, e.g., exports and

investment. The impact of GEM is, however, also affected by the slope of

the Aggregate Supply Curve. If AS is elastic GEM will be large; if AS is

inelastic, small. This is a matter of professional controversy in

economics.

b) Autonomous

Tax Multiplier (ATM)

There are essentially two kinds

of taxes - induced and autonomous. Induced taxes rise and fall as real GDP

varies. The change in tax revenue is determined by the 'fixed' marginal tax rate

(MRT). Taxes increase or decrease as real GDP changes. In this way they

act as an automatic stabilizer,. i.e., if GDP grows then taxes increase

and transfer payments decline; if GDP declines then taxes fall and transfer

payments increase.

Autonomous taxes do not vary with

real GDP rather they are fixed by Government. An increase in taxes decreases

disposable income and hence consumption and therefore aggregate expenditure.

But the decrease in AE will be greater than the increase in taxes (P&B 4th

Ed

Fig. 26.9). The size of the ATM depends on the slope of the AEC

and, hence, of the MPC. ATM = -b/1-b =

∆Y/∆T.

If MPC is .75 then ATM is .75/1-.75 = 3 compared to 4 for GEM. This means

that a tax change has a smaller multiplier impact than an autonomous expenditure

change of the same nominal amount. This is because all of an autonomus

expenditure is spent immediately while a decrease in autonomous taxes is only

partially spent and partially saved (MPS).

The inverse of the ATM is the multiplier associated with transfers. Transfers

are like negative taxes, i.e. taxes are reduced. Another related concept is 'tax

expenditures' where Government selectively reduces taxes and losses revenue

thereby. The autonomous transfer multiplier is simply the negative of the ATM.

c) Balanced

Budget Multiplier (BBM)

The BBM is the amount by which a

simultaneous and equal change in government expenditures is matched by a change

in autonomous taxes. The result is that the initial balance between government

revenue and expenditure (deficit/surplus) is maintained. The BBM requires that the

effect of GEM

(1/1-b) should exactly offset the effect of ATM (-b/1-b) so that ∆Y/∆G

= - ∆Y/∆T

d)

Impact of Marginal Propensity to Imports (MPM)

If we assume a MPC of .75, i.e., 75 cents of every dollar is spent on

consumption then the GEM is 1/1-.75 = 1/.25 = 4. If, however, the MPM is

.1, i.e., 10 cents on every dollar is spent on imported goods then GEM is

1/1-.75-.1 = 1/.65 = 2.86. This compares with a closed economy GEM of 4.

e) Automatic Stabilizers vs. Discretionary Changes

(MKM

C15/406-8; 381-82; 400-401)

The Keynesian model does not rely only on discretionary fiscal

policy. As noted in the

introduction

to this section, discretionary policy can suffer from 'policy lags' leading to

counterintuitive effects, e.g., fiscal stimulus is implemented but its

impact occurs to late just as the business cycle turns around and then over

stimulates the upswing. On the other hand, automatic

stabilizers are triggered by 'objective' changes in the economy and implemented

automatically according to an existing legislation, e.g., in a downturn,

unemployment rises, employment insurance payments increase maintaining aggregate

demand and on the upswing payments into the unemp0loyment insurance fund

increase while outflows diminish. Similarly in a downturn causes income to

fall and marginal taxes decrease. Welfare and other public programs

automatically kick in during a downturn and decline in the upswing. A

flexible exchange rate similarly buffers domestic aggregate demand. During

the upswing of the business cycle Canadian prices, especially interest rates,

start to rise. Rising interest rate attracts foreign investment that

requires the purchase of Canadian currency increasing the foreign exchange rate.

Canadian exports become more expensive on world markets reducing exports and

thereby reducing aggregate demand. On the other hand, during a down turn

Canadian interest rates tend to fall and foreign investment declines as does

foreign demand for the Canadian currency thereby reducing the foreign exchange

rate. This makes Canadian exports less expensive and they increase thereby

boosting domestic aggregate demand.

iii - Short

& Long Run Fiscal Policy

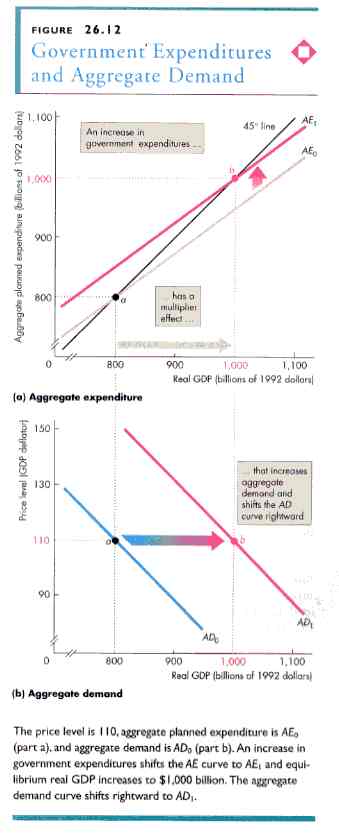

a) Aggregate Demand

Assuming price stability, an

expansionary fiscal policy (an increase in government expenditure, an increase

in transfers or a decrease in taxes) will push aggregate planned expenditure up

by the change times the appropriate multiplier. This will lead to an increase in

aggregate demand at the same price level and reflected in a shift to the right

of the aggregate demand curve (P&B 4th Ed

Fig. 26.12). Similarly, assuming price

stability a contractionary fiscal policy involves a decrease in government

expenditure, a decrease in transfers and/or an increase in taxes. This will lead

to a decrease in aggregate demand at the same price level times the appropriate

multiplier and reflected in a leftward shift of the aggregate demand curve.

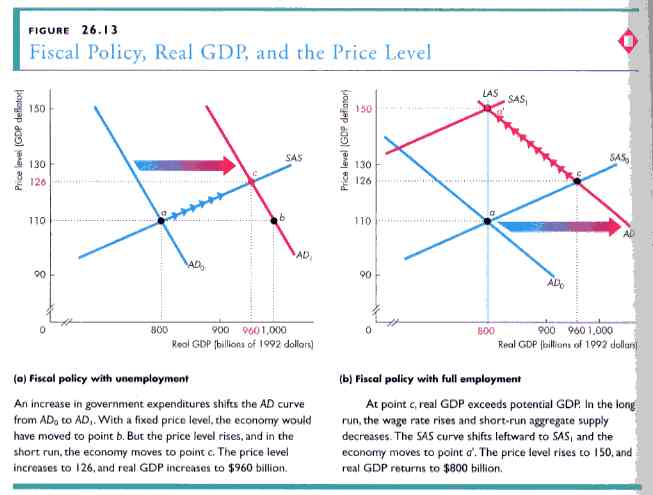

b) At or Below

Potential GDP

If the economy is below potential

GDP then there is some unemployment. The rightward shift of the ADC will,

however, intersect the ASC at a higher point. Thus some of the initial increase

in AD will inevitably translate into a general price rise reducing the overall

effect of an expansionary fiscal policy (P&B 4th Ed

Fig. 26. 13). If the economy is

at potential then all the effects of an expansionary fiscal policy must fail in

that there is no increase in real GDP possible and the only change has been an

increase in the price level.

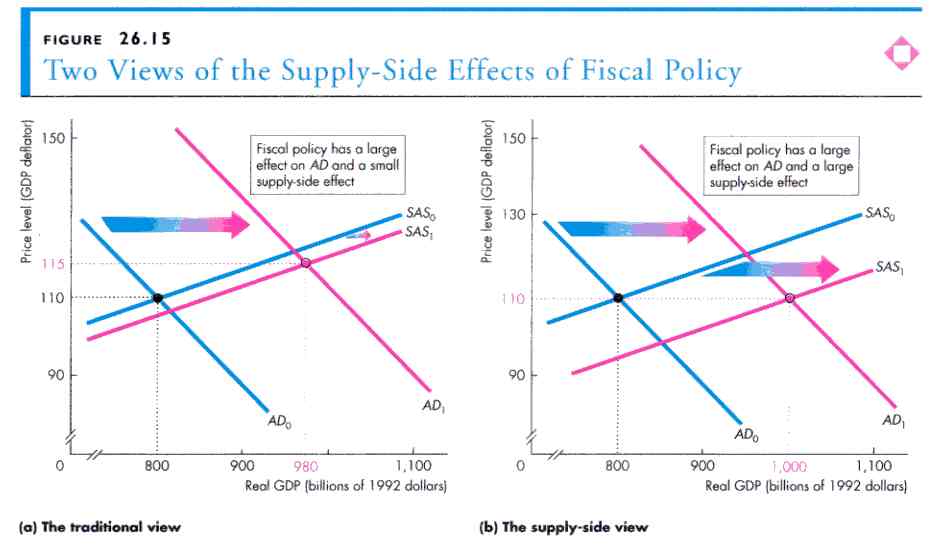

c) Aggregate Supply

While traditionally Keynesian theory

has focused almost exclusively on aggregate demand as a means of moderating the

business cycle and foster economic growth and price stability, a logical

extension leads to the supply-side. Taxes are treated as part of the price of

factors of production by firms. Accordingly, if taxes rise the cost of

production goes up and the ASC shifts to the left. Similarly, if taxes fall then

the ASC will shift to the right, in effect increasing potential GDP (P&B 4th

Ed

Fig. 26.15). Thus taxes have an effect on both AD and AS.

This is known as 'supply-side economics'. While tax reductions may have a

supply effect the fact is once taxes effectively reach zero this policy tools

loses any effectiveness.

d) Deficit & Debt

-

more like business

- balance sheet

- capital/operating and amortization

- trans-generational transfers

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}