|

Observation #0: Origins

Observation #1: The Wealth of Nations

Observation #2: The Economics of Democracy

Observation #3: Capital, Labour & Natural Resources

Observation #4: Technological Change

Observation #5: Fiscal Policy in Canada

Observation #6: A Brief History of the Central Bank: UK, USA & Canada

Observation #7: Shadow Banking & the Great Recession of 2008

Observation # 8: Jeremy Bentham

Observation #0: Origins

The Standard Model of Microeconomics (or

Market Economics), specifically 'X' marks the spot, was formalized by

Alfred Marshall at Cambridge University at the end of the 19th and early

part of the 20th centuries. He provided the solution to profit

maximization under perfect competition and monopoly. In the 1930's Joan

Robinson, also at Cambridge, provided the solution for monopolistic

competition but in an interesting intellectual coincidence it was

independently resolved, at the same time, by Edward Chamberlin in the

U.S.A. As will be seen, the Standard Model was then extended into

Welfare Economics (including Externalities) by Arthur Cecil Pigou who

succeeded Alfred Marshall in 1908 as Professor of Political Economy at

the University of Cambridge holding the post until 1943. Thus the

Standard Model of Market Economics could more accurately be called 'The

Cambridge Model'.

Its roots, however, lay in the 'Marginalist

Revolution' of the 1870s. This shifted the focus of economics from the

production and distribution of wealth among social classes - owners of

capital, labour and natural resources - towards the atomized individual

consumer (2.0 Demand) and producer (3.0 Supply). Microeconomics was born

- the budget constrained maximization of consumer happiness and the cost

constrained profit maximization of producers underpins the standard

model.

This Standard Model of Market Economics

served as the foundation for development of the Standard Model of

Macroeconomics by John Maynard Keynes (also of Cambridge) with his 1936

The General Theory of Employment, Interest and Money. Until then

government did not play an active role in managing the economy. Rather,

it was governed by 'the iron law of wages'. As the economy boomed

labour became scarce and wages rose until the economy crashed. As the

economy declined labour was increasingly unemployed and wages fell until

low enough to jump start the economy. There was no government

intervention, no 'social safety net'.

Observation #1: The Wealth of Nations

0.

Introduction

What is wealth? What is a nation? And, accordingly, what

is 'the wealth of nations'? Through time the meaning of these

terms has and

continues to change and mutate.

a) What

is a Nation?

First,

what is a Nation?

I will restrict myself to the

Western European and especially of the English experience which I have

studied in some detail. I thereby confess my relative

ignorance, i.e., lack of knowledge, of the evolutionary

experience in other regions of the world.

From Tribe to Empire & Back

Once upon a time a Nation was a 'tribe'. A people of the same ethnicity, language and religion - a

whole people but one often made up of different clans. Ancient Egypt, China, Persia and Greece were such

nations; anyone outside was 'a barbarian'. Rome, on the other

hand, began as a tribe - the Latins - but ended up an Imperium in

which citizenship was not limited by blood, birth, language or

religion.

The

modern Nation States of Europe recapitulated Rome beginning as

Germanic and other tribes - Bavaria (Bavarians), the Burgundians (Burgandy), the Franks (France), the Helvetica (Switzerland),

the Lombards (Lombardy), the Swabians (Swabia), the Saxons (Saxony),

the Magyar

(Hungary) and the Russ (Russia). Some then collasced and evolved

into European colonial empires transformed after WWI into Nation States

(a term not introduced into American English until 1919) and more

recently into

the pan-national

European Union, sometimes called the second Roman Empire.

England

From Divine

Right to Throneworthiness

Along

the way, a related question arises. Is a Nation a land, a

people or a king or queen? David was anointed King

of Israel.

So says the Old Testament. This served, in the West, as the basis

for the

Divine Right of Kings. The Church of Rome,

however, separated the secular powers of the King (or Emperor) from the spiritual

power given to St. Peter by Christ in the New Testament: "Pay unto

Caesar what is Caesar's and unto God what is

God's". The opposing principle called caesarpapism

merged the spiritual and secular roles in the Eastern Roman

or Byzantine Empire. Henry VIII of England

reverted to caesarpapism by returning the spiritual power to the King as

head of the Church of England in 1534. One implication

of the Nation as Monarch was that through marriage the

territorial limits of a nation could, and often did, change. A more extensive description is available in

my article:

Christianity,

Censorship and Copyright in English-speaking Cultures.

However,

the people of England during its Civil War (1642-1651) answered

the 'Divine Right of Kings' in 1648 by beheading King Charles

I and starting the first modern republic, the short-lived

Commonwealth of Oliver Cromwell.

The argument was based on the ancient Anglo-Saxon law of

throneworthiness. Kings were elected according to how much

rape, pillage and spoils they could deliver (MacDougall

1982). Ironically 1648 was also the year in which the

Treaty of

Westphalia (actually a series of treaties ending the

Thirty Years War)

was signed. In brief, it birthed the modern Nation-State as a

sovereign geographic entity in which minority religious rights of

Christians - Protestant or Roman Catholic - were secure from secular and

religious persecution. Non-Christians had to wait until the mid-20th

century.

From the

Scientific to the Republican Revolution

The Commonwealth (1649-1660), however,

was followed by the

Restoration of the monarchy in 1660

becoming a constitutional monarchy with

the

Glorious Revolution of 1689. These

events were accompanied by the

Scientific Revolution. Unlike

other European states, England during the

Reformation split not two but three ways –

Protestant, Catholic and Anglican or Church of England. It was in these

troubled times that

Francis Bacon

in his 1605 Of the Proficience and Advancement of Learning Divine

and Humane began his call to Scholars to come down

from their ivory towers into the workshops of Mechanics to practice the

instrumental experimental scientific method and force Nature to reveal

her secrets. Fifty years later at the height of Cromwell’s Commonwealth

Robert Boyle provided the metaphysical rationale for this new

‘experimental philosophy’ placing the laws of the Nature in stasis

above and beyond human and divine intervention. God having created the

world set His Laws in motion and withdrew, no more miracles or divine

intervention. He left, however, a second book, the

Book of Nature, that had to be red and all of Nature was therefore the legitimate subject of experimental

philosophers. This was the ‘Latitudinalist compromise’ (Jacob

1978). Its logo was Newton’s clockwork universe running on the

calculus of motion. Secular and religious legitimacy for

experimental philosophy was granted by Charles II's charter to the Royal Society

of London for the Improvement of Natural Knowledge in 1662 (Jacob

1978;

Jacob & Jacob 1980). Theologically, this Revolution

placed the material world beyond the opinion of popes, priests and

philosophers. No longer would hot or cold be determined by the

personal whim of a superior but rather by the thermostat. The

machine became the measure of all things physical leading to Instrumental Realism (Idhe 1991).

The first successful Republican

revolution was the American of 1776. It overthrew an ancient regime of

subordination by birth but nonetheless adopted many of the Common Law

legal traditions and precedents of their ancient masters especially

business law and most importantly, intellectual property rights like

copyright, patents and trademarks.

Henceforth, however, the individual, not the family, clan or

bloodline would be the lodestone of society. This marked the

culmination of a process beginning with the

artist/engineer/humanist/scientist of the 15th century European

Renaissance. The individual through creativity and talent erupted out

of anonymity into celebrity. It continued during the Protestant

Reformation of the 16th century when the individual was linked directly

to the godhead without intermediation by pope, priest or philosopher.

It accelerated with the Scientific Revolution of the 17th century with

the ‘experimental philosopher’ who William Whewell, at the request of

the poet Samuel Coleridge,

renamed ‘scientist’ in 1833 (Snyder 2000) and continued with the

'author' in the 18th century, the 'inventor' in the 19th and the

business 'entrepreneur' of the 20th century. This is known as the western

Cult of Genius.

The second Republican revolution,

the French of 1789, threw out not just feudal overlords but also common

law and religion. The French Revolutionaries re-thought Law from a

Republican, secularist perspective. Like the Americans, they made the

Individual, the Natural Person, the cornerstone of the political and

social order. Thus the American Declaration of Independence announces:

“We hold these truths to be self-evident, that all men are created

equal, that they are endowed by their Creator with certain unalienable

Rights, that among these are Life, Liberty and the pursuit of

Happiness”. The French Declaration of the Rights of Man and the Citizen

of 1789 (Article 2) arguably goes further declaring: “The aim of all

political association is the preservation of the natural and

imprescriptible rights of man. These rights are liberty, property,

security, and resistance to oppression.” [emphasis added]

The term natural indicates that Nature, not some

divinity, is the scientific source from which these rights flow in an ideological

sense. The word ‘ideology’ has many meanings today (Gerring 1997) but

was coined simply enough by Condillac in 1797 to mean ‘the science of

ideas’ (OED, ideology, 1b). Separation of Church and State was critical

to both American and French revolutionaries but the French were atheists

while the Americans were theists. A secular science of ideas to counter

the awe and mystery of religious and metaphysical thought and ritual was

part of the French revolutionary agenda to complete the overthrow of the

ancient regime.

In this sense an ideology is a 'secular' theology explaining the

way the world works but without any necessary reference to a divinity.

The

term imprescriptible indicates that no contract infringing such

rights, even willingly signed, is enforceable by the courts, i.e., they

cannot be signed away. They cannot be assigned, transferred or waived in favour of a Proprietor – Natural or Legal. The difference between

Anglosphere Common Law and (what began as the Napoleonic Code but

evolved into) the European Civil Code with respect to intellectual

property is arguably one of the hottest international trade

controversies - Disney vs. France, the United States vs. the 2005 UNESCO

Convention on Cultural Diversity, etc. As I argue

elsewhere, with respect to intellectual & cultural property the American is an

unfinished Revolution. Please see my

Preface: Intellectual & Cultural Property - Cult of the Genius.

There was in fact five major waves to the Republican

Revolution: (i) the English

Revolution or ‘Great Rebellion’ of 1640; (ii) the American

Revolution of 1776; (iii) the French of 1789; (iv) the Latin

American Bolivian Revolution of the early 19th century; and, (v) Sun Yet Sen's Chinese

republican revolution of the early 20th century. In all cases

they were betrayed. In the first, the monarchy was

restored in 1660 and the ‘Glorious Revolution’ of 1689 was

required to establish a ‘constitutional’ monarchy. In the

second, the definition of ‘Man’, or Natural Person, was limited

to white males (sometimes called the ‘pale penis people’). In

the third, terror was justified in the defense of liberty. In

the fourth, a caste system - with descendents of European

conquistadores at the

top, mixed bloods in the middle and indigenous peoples at the

bottom - was erected. And the fifth was swept away by the

Communist Chinese Revolution of 1949.

Progressively, however, the franchise has been extended to all

Natural Persons as citizens, discrimination under the law has

been progressively eliminated and the concept of human rights

become engrained

into the polity.

The concept of 'a

republic', of course, dates back to ancient Greece and Rome. The

modern republic, however, is grounded, more or less, not on common ethnicity, language or religion, but on

'the people' as a whole including all those born within the territorial

limits

of a Nation State (even the children of immigrants). Today,

the vast majority of humanity takes for granted that 'the people'

constitute the Nation even if a 'constitutional monarch' wears a token Crown. This

is the triumph of democracy. Furthermore, with

the end of the Market/Marx Wars the Communist Revolution

collapsed. The previous Republican Revolution survives and a

world divided and threatened with nuclear winter for almost half

a century because of a domestic feud between two schools of

economic thought now rallies around the last ideology standing – market

economics with its political and legal corollaries: popular

democracy and private property.

For our purposes

macroeconomics functions at the level of the Nation State.

For further information about the shifting sands of sovereignty on which

it stands, please see: Chapter

13.0 The Nation-State, of my dissertation

The Competitiveness of Nations in a

Global Knowledge-based Economy.

b) What

is Wealth?

If

the meaning of Nation has changed through time, the meaning of wealth

has also transformed. The

common meaning of the word wealth as given by the Oxford Concise

Dictionary is: n. riches, large possessions, opulence; being

rich; abundance; a profusion or great quantity or display. A

subtext to the definition, however, is more revealing. By subtext, I mean, in this case, the etymology or

origin of the word. In the case of wealth the

OED says: Middle English from well and weal, after health.

And hence the concept of the 'commonwealth'.

In

a subsistence 'hunter gatherer' economy, wealth is easily defined.

In very simple terms, anyone with lots of food and other requirements

for survival is wealthy; anyone without is poor (and usually unhealthy and

soon dead). The Agricultural Revolution generated a significant

surplus in the food supply permitting a higher order of

division and specialization of labour than possible in a hunter gatherer society. Wealth began to

include not just the necessities but also 'luxuries' like jewelry,

precious stones and metals as well as land, skilled craftspersons and

great buildings. An often overlooked parallel to the Agricultural

Revolution was the 'Maritime Revolution', e.g. of the Amerindian culture

of the northeast coast of North America (known as the

Maritime

Archaic

culture) which 7,000 years ago enjoyed a significant food surplus through

command of the seas. It has even been suggested that

they sailed to Europe. With the Industrial Revolution

and steam power, the

concept of wealth changed yet again. This time it expanded to

include manufacturing facilities vastly more complicated and diverse than

the water and wind mills of the Agricultural Revolution and, in a sense,

beyond human scale. It

also ushered in a new form of wealth in the form of equity shares in

limited liability corporations rather than outright ownership.

c) What

is the Wealth of Nations?

Until the 1930s there was no 'macroeconomics'.

There was no 'national economy'. In

effect, there were two relatively disconnected sectors: government (the monarch

and/or Parliament) and the private sector (the people). The

economy went up and down ruled by the

iron law of wages. As the economy boomed labour became scarce and wages

rose until the economy crashed. As the economy declined labour was

increasingly unemployed and wages fell until low enough to jump start

the economy. There was no government intervention, no 'social

safety net'.

Here is a timeline for the changing

meaning of the wealth of nations:

i -Mercantilism: 16th to 18th Century

At first this disconnect reflected the vision of the

Nation

as the private concern of a monarch and was 'proprietary' in nature. The

monarch or Parliament was politically 'absolute' and economic policy was

Mercantilist.

How much gold, silver, land and slaves (or serfs) was the measure of national

wealth. Sell as much and buy the least from foreign countries and build up

ones bullion reserves. The people consisted of serfs, slaves, servants,

commoners, soldiers and vassals

or aristocrats - dukes, counts, barons, etc - who swore allegiance to the monarch

who, in turn, made demands of, and granted privileges to them. National

economic policy consisted, initially, of Crown grants of monopoly privilege to the

monarch's favorites to fund the monarch's scheme,

palaces, ventures and wars while taxes approved by Parliament were levied on the

general population - including a head tax - to finance domestic peace, order and

good government. Little concern was given to the well-being of 'the

people'.

ii -

Classical: 1776 to 1870's

By the end of the 18th century,

democratic government - constitutional monarchies and republics - arose. However, in response to the excesses of monarchial

interference with the economy during the

Mercantilist

period,

laissez

faire (let the entrepreneur decide what to produce and not the Crown) &

laissez passer (let workers move to work where they want, not to where guilds assign them) became the norm, that is, limited involvement by government

in the economy. The central economic concept, however, remained 'class' and the

question was the division of national income among the classes. Thus, on

the one hand, the politics

of the Republican Revolution made the individual as voter the foundation of

the polity, in

classical economics class remained the primary unit of analysis.

It was also believed that the market would self-adjust

the business cycle. The mechanism of adjustment was called the Iron Law of Wages. If workers earned more they would simply breed increasing the

number of workers and thereby forcing wages down to a subsistence level.

If wages were too low, workers would not reproduce reducing the number of

workers forcing wages up which, in turn, would lead to more workers with wages

again falling again to the subsistence level and so on.

By the mid-19th century 'Socialism'

arose. Beyond Karl Marx & the Boys (Lenin, Stalin, Mao,

Fidel, Pol Pot, et al), however, there are many forms of socialism

with differing views of the relationship between 'the working class' and the rest

of society. The history of the Labour Movement demonstrates such

differences, e.g., the

Knights of Labor. the Industrial Workers of the World or "Wobblies",

Fabianism with its concept of Industrial Democracy, Syndicalism, Gomperism

or business unionism,

etc.

What they share in common is a focus on class - the working class hero

of John Lennon - not the

individual.

iii - Neo-Classical: 1870 to

1936

Beginning in the 1870s the

Marginalist Revolution

in economic thought made the atomized consumer and

producer maximizing utility and profit, subject to the constraints of budget and

price/cost. Its vision could be expressed in

deductive logic based on simple assumptions and demonstrated in words,

calculus (numbers) and geometry (graphs) satisfying Descartes'

definition of a 'science'. It represented the marriage of the

felicitous calculus of Jeremy Bentham and Newton's calculus of motion.

In many ways it is the economic flip-side of the Republican Revolution

doing away with 'class' in classical economics including Marxism and

replacing it with the atomized constrained maximizing individual as

consumer/producer. It also explains, among other things, why

the Market/Marx Wars ended the way they did. It is the individual,

not class, that matters because we are always both

consumer and producer. For more information, please see my

notes on

The Marginalist Revolution.

It was, however, the height of the

European colonial empires that remained Mercantilist internationally

with a laissez-faire domestic market. These attempted through colonies to

become self-sufficient with respect to resources and markets. They

strived for

autarky. No truck nor trade with the enemy unless absolutely

necessary.

iv -

Keynesian 1936 to 1970s

Belief in the

self-adjusting power of the marketplace continued to dominate economic thinking

until the

Great

Depression of the 1930s. The economies of the industrialized world did

not self-adjust to the first synchronous global downturn. Before if

Germany was depressed France was inflated or if Britain experienced a downturn

the the U.S. boomed while Japan continued to industrialize and joined the crowd.

All national economies sank at the roughly the same time. Unemployment was very high (25-30%); social

unrest and revolution was in the air. Many considered that

Fascism

in Italy,

Nazism

in Germany,

Communism

in Russia and the Imperial Japanese 'Co-Prosperity Sphere' offered answers to the suffering of the

people. All were essentially authoritarian, racist and totalitarian

in nature. In this sense the Second World War was in fact as much a war

against racism as fascism. Furthermore, like the European colonial empires

on which the sun never set, they advocated autarky rather than the

comparative advantage of international trade

to

answer the global economic crisis. In this regard, the Cold War

represented a similar attempt to attain autarky - no truck nor trade with the

Commies or Capitalists, depending in which Bloc one lived.

The liberal democracies desperately sought an

alternative. In politics, the United States elected

Franklin

Delanor Roosevelt as President in 1933 on the platform known as the 'New

Deal'. In economics,

John

Maynard Keynes offered a new view of the economy requiring government to

play an active role without exerting ownership or requiring corporatist

dirigisme and retaining the free market as the primary economic institution.

Macroeconomics

was born. It is Keynes' model that we will examine in this class. It

is arguably the 'standard model' of macroeconomic thought because even its

critics use the same instruments of analysis introduced by Keynes and his

successors. It focuses not

on class or the individual consumer/producer but rather on functional aggregate

categories such as households, consumption, savings, investment, government expenditure,

etc. For more information, please see my

notes on

The Keynesian Revolution.

v - Post- Keynesian

1970s to ?

By the late 1970s Keynes' belief in

government's ability to 'fine tune' the economy and the efficacy of its

'fiscal policy' - tax and spend - was questioned for reasons discussed

later in this course. The policy focus shifted to the Monetarists who

emphasized the role of the central bank in manipulating the money supply

and the cost of money or the interest rate (r) to fine tune the

economy. Similarly, fiscal policy was seen as inherently

limited by the Rational Expectationalists who took exception to Keynes'

key assumption about workers' price expectations resulting in sticky money wages -

a subject to be discussed later in the course. With the recent

'Great Recession', however, a mixed Keynesian/Monetarist economics is

being tested: Can brute monetary intervention together with limited government

expenditure stimulus prevent another Great Depression? Its

competitor is the the Austrian School of von Hayek and von Mises that

argues the economy should simply be allowed to clear out bad investments made by

producers and consumers with no government intervention. Another critical difference with the 1930s is there is no viable

ideological alternative to market economics. It is the last

ideology standing.

2.

Global Knowledge-Based/Digital Economy

Please see the linked

historic exhibit.

Please see my

recent article:

Disruptive Solutions to Problems associated with the Global

Knowledge-Based/Digital Economy. Please see

my dissertation:

The Competitiveness of Nations in a Global Knowledge-Based Economy.

More will be said about this emerging economy and the role of

intellectual property rights (IPRs) - copyright, patent, registered industrial design,

trademark, 'know-how' and trade secrets - later in the course.

Arguably, IPRs represent wealth in the global knowledge-based economy.

Unlinked Reference

MacDougall,

H.A., Racial Myth in English History: Trojans, Teutons and

Anglo-Saxons, Harvest House, Montreal,

1982.

Observation #2: The

Economics of Democracy

Keynes believed that the business cycle reflected the

fickle 'animal spirits' of investors alternating between Fear & Greed.

He called on Government to compensate for these mood swings relying on

'the multiplier'. But how stable is the mood of Government?

Can it be relied upon to make sober, sensible decisions? Is it, in

turn, subject to 'animal spirits'?

There are three actors in the economics of democracy:

voters, politicians and bureaucrats. Each has its own 'objective

function' which its strives to maximize subject to constraint.

Ideologically every polity can be characterized by colours in two

dimensions. Horizontally, there are Blues - conservatives,

monarchists, fascists, etc. and then there are Reds - liberals, social

democrats, communists, etc.. Vertically there are Browns -

techies, engineers, mechanists, etc. and, then there are Greens -

ecologists, nature lovers, romantics, etc. One can thus have Red

Greens (Green Peace) as well as Blue Greens (Sierra Club); Red Browns

(Communist apparatchiks and nomenclatura) and Blue Browns (Nazis

technicians 'just following orders'). At the extreme, one can also

have Blue Reds when far Left (e.g., the Party as vanguard of the

revolution) turns into far Right (e.g., the dictatorship of the

proletariat) or vice versa.

Arguably the seminal text in what today is called 'rational

choice theory' was published in 1957 by

Anthony Downs: An Economic Theory of Democracy. Other

economists have followed as have other disciplines including Law and

Political Studies. For our purposes there are three primary

actors in the public policy process:

i -Voters;

ii - Politicians; and,

iii - Bureaucrats.

i - Voters

The objective function of the voter is maximizing

utility when that function includes Equity, Externalities and Public Goods. They are constrained primarily by what

is alternatively called Rational

Apathy

or

Ignorance.

If one is to be an informed voter one must learn about the issues - time

& effort. Having determined the issues one must then decide where

one stands - time & effort. Having decided one must chose the

politicians who reflects one's views - time & effort. Having

selected the candidate one must get out and vote - time & effort.

Time & effort represent costs to the voter who unless strongly motivated

is rational to be apathetic and stay ignorant of the issues and stay at

home on election day. This is why we say a government is not

elected but rather defeated. Thus in federal elections only about 60%

turn out to vote; in provincial elections only about 50%; in municipal

election about 10%; and for school and hospital board elections only

about 1% get out and vote. This has significant

implications. Taking just the federal level it means that 30% of

the electorate can elect a majority government which can use the

'notwithstanding' clause to abrogate any of those rights and freedoms in

spite of the courts. The same

'notwithstanding' clause

holds for the Provinces but where

only 25% can elect a majority government. This reflects what

Jeremy Bentham called "legislative omnicompetence" - the supremacy of

the House of Commons under Parliamentary democracy.

Another characteristic of voters (and citizens in general)

is adverse selection. This is most apparent in the case of

insurance. Adverse selection occurs when one's demand is related to one's risk but

the insurer cannot adjust pricing. This may occur

because risk information is known only to the individual (information

asymmetry), or due to regulations or social norms

preventing the insurer from using certain information to set

prices, e.g., gender, ethnic origin, genetic test

results or preexisting conditions. The latter case it is

called "regulatory adverse selection". Thus if an insurer does not

vary prices according to smoking status, life insurance is a better buy

for smokers than for non-smokers and smokers will be tend to buy more

insurance than non-smokers. For the insurer the higher mortality

of smokers is adverse. Something similar happens in politics.

If one is unemployed one will tend to vote for the politician promising

government intervention which raises the cost of government.

Yet another characteristic is moral

hazard.

Economist

Paul Krugman describes moral hazard as "any situation in

which one person makes the decision about how much risk to

take, while someone else bears the cost if things go badly." For example, bank

bailouts by governments, central banks or other

institutions may encourage risky lending in future because those taking

the risk believe that they will not have to bear all the losses.

Fire insurance is another example. One buys fire insurance to

cover losses but by insuring against fire one may be tempted to commit

arson to collect the insurance payout. Politically, similar

problems have been associated with government programs as noted by

Rational Expectationalists, e.g., the American urban homesteading

program.

ii - Politicians

The objective function of politicians is to get elected or

re-elected. They are constrained primarily by Arrow's

Impossibility Theorem.

If a politician receives 51% support on every issue in an election

campaign that politician looses the election! Why? Rational

Apathy. The 51% comfortable with the politician's position tend to

stay at home in large numbers while the 49% opposed are motivated and

turn out and vote. Again this is why we

say a government is not elected but rather defeated.

This encourages politicians to take a

middle-of-the-road position on most issues thereby avoiding painting a

target on their backs. Similarly political party platforms tend to

avoid alienating voters by taking

a middle-of-the-road position,

until Trump. Edifice Complex

iii - Bureaucrats

The objective function of bureaucrats is 'steady as she goes',

'no waves'. The bureaucracy should run like a fine tuned engine.

There are two distinct types of bureaucracies - political and

professional. In the U.S. all positions from the director level to

Secretary of State are political appointees. Each serves at the pleasure

of the sitting President. This is part of the political spoils

system. It is relatively easy to appoint loyalty over competence.

In the parliamentary democracies like Canada there is a profession

public service that fill positions from clerk up to deputy minister.

Theoretically competence is valued over loyalty to the party in power.

In both cases bureaucrats are constrained by politicians and voters.

It is, however, of the parliamentary democracies of which I coined the Three Laws of Technocracy.

Two qualifications: first, they are based on my career experience;

second, the term 'technocracy' was coined by

John Kenneth Galbraith to explain large

corporate bureaucracies. To the degree competence is the

test in both the following apply to both.

The bureaucrat can relax the constraints in three ways:

Confuse & Conquer

A minister in government is generally

not

a specialist in the subject area. The professional

bureaucrat usually is. When the politician proposes a new policy

that will make waves for the bureaucracy the bureaucrat can make the

question so complicated that the politician backs off or leaves it to

the bureaucrat - confuse & conquer. The self-regulating

professions are similarly capable of making an issues so complicated the

client leaves it to their better judgment.

What We Don't Know Won't Hurt Us

For all the talk about freedom of information the reality

is the bureaucrat and the politician often practice 'What we don't know

won't hurt us!' With information politicians and voters may ask

questions that require the bureaucracy to answer creating waves and

causing the fine tuned engine to stutter. If information is simply

not collected then questions cannot be asked and therefore there is no

need to answer. No waves. No stutter. Real world

examples abound!

When in Doubt Privatize

One aspect of parliamentary democracy is

the role of the Auditor General who is an officer not of Her Majesty,

i.e., the executive branch, but rather an officer of the House of

Commons. The office was originally established to ensure that tax

revenues authorized by the House were used

by the Crown for their voted

purpose. If, however, a Crown Corporation is established

or an activity is privatized but financially supported

by the government

then the cloak of commercial confidentiality falls over

its financial operations and the Auditor General usually does not have

authority to check the books. In fact the most powerful form of

privacy in a capitalist system is commercial

confidentiality.

Observation #3: Capital, Labour & Natural Resources

Capital (K)

The

definition of capital is an unresolved problem in economics. To Marxists, it is

theft. To the mainstream, its definition remains problematic as noted by T.K.

Rymes of Carleton University in conversation with the author in the early 1970s:

“If there is no theory of capital, there is no economics. And there is no

theory of capital!”

The concept of capital has

mutated and expanded through history. To the Mercantilists of the 17th century,

capital was gold, silver, land and slaves. To the Physiocrats of

pre-Revolutionary France, it was the surplus generated by agriculture. To the

Classical School of the late 18th and early 19th centuries, it was the surplus

resulting from the division and specialization of labour. To the Neo-Classical

School of the late 19th and 20th centuries, it was financial capital as well as

physical plant and equipment. To Bohm-Baverk and

the Austrian School, capital was historically embodied labour produced through

‘round-about’ means of production (Blaug 1968, 510-11). How to measure such

embodied labour has never, however, been satisfactorily answered (Dooley

2002).

Today, when

economists speak of capital, they may refer to cultural, financial, human,

legal, physical, social or other forms expressed as a stock, e.g.,

physical plant and equipment existing at a given moment in time.

For my purposes, capital is codified and tooled

knowledge, i.e., knowledge fixed in an extra-somatic matrix.

Alternatively, capital is “knowledge imposed on the material world” (Boulding

1966, 5), or, “frozen knowledge” (Boulding

1966, 6). It includes:

codified knowledge in the form of human-readable

information management systems and databases, operating manuals and libraries as

well as associated intellectual property rights such as copyrights, patents,

registered industrial designs and trademarks; and,

‘hard-tooled’ knowledge in the form of physical

plant and equipment, i.e., sensors and tools, plus related ‘soft-tooled’

knowledge including machine-readable computer & genomic programs, standards and

techniques.

Codified and tooled knowledge are fixed in material

form; both have vintage; both are extra-somatic, i.e., they exist outside

the natural person. I will now briefly examine softer forms of capital -

cultural, financial, human, legal and social - expressed as codified and tooled

knowledge.

Cultural

Cultural capital, as artworks, books, photographs,

plays, recordings, etc., is codified knowledge. As broadcast & recording

studios, conservatories, libraries, museums, parks, printing presses, sets,

props & costumes, theatres and other venues, it is tooled knowledge. In this

sense, cultural capital (codified and tooled) contrasts with cultural practice

or performance which is personal in nature.

Financial

Financial capital as currency, equities, bonds,

mortgages and other financial instruments is codified knowledge, i.e.,

fixed on paper or in human readable electronic format. Anti-counterfeiting

measures such as encryption, electronic strips and chips are forms of tooled

knowledge. Debit and ‘smart’ cards are contemporary examples of financial

capital as tooled knowledge. In this view, financial capital (codified and

tooled) contrasts with financial practice which, again, is personal in nature.

It is as personal & tacit knowledge, however, that

financial capital plays its primary role. As a generally accepted medium of

exchange, store of value or unit of account, financial capital as money involves

tacit knowledge routinely recognized and accepted by a natural person. In this

sense, financial capital, including the price system (Hayek

1989), is an institution, i.e., a routinized pattern of

collective human behaviour. Like a physical reflex, e.g., riding a

bicycle, a human being learns to recognize, accept and exchange financial

capital. In different cultures and periods of history what constitutes money

and financial capital differs (Humphreys 1969). In other words,

financial capital is a cultural artifact, a form of organizational technology

that is tacit, i.e., ‘generally accepted’ in a society.

Human

Human capital generally refers to the stock of skills

and education possessed by a worker. Given human capital is embodied in a

living human being, there is no extra-somatic component, i.e., there is

no capital as frozen knowledge. The term ‘human capital’ is thus a misnomer.

Human capital is personal & tacit knowledge and somatic to the individual.

Additions to this stock reflect learning, education, experience and training on

the memory and reflexes of the individual.

Legal

Legal capital as law books, statutes, judicial and

quasi-judicial decisions is codified knowledge. Legal capital as court houses,

handcuffs, prisons and police cars is tooled knowledge. In this view, legal

capital (codified and tooled) contrasts with legal practice which is personal knowledge.

Social

Social capital can be codified and fixed on paper or

another human-readable format stating customs and conventions of behaviour,

educational curricula, public rules and regulations as well as public safety

standards, e.g., drinking water standards. Social capital as schools,

hospitals, roads, sewage & water systems and telecommunication systems is tooled

knowledge. In this view, social capital (codified and tooled) contrasts with

social practice including market sentiment which are persona knowledge.

Social capital, according to some

scholars, can be extended to include “values and beliefs”. Such values and

beliefs can be codified, e.g., the Analects, Bible, Koran & Vedas.

Alternatively, they can be tooled into monuments and other works of aesthetic

intelligence reflecting an ideology, e.g., socialist realism. Values and

beliefs, however, take on meaning only when practiced or perceived by a living

human being. In this sense, there is no extra-somatic component, i.e.,

there is no capital or asset that can be exchanged for money. Put another way,

“Money can’t buy you love”.

With respect to economics, such values and beliefs

include market sentiments. In The Theory of Moral Sentiments and The

Wealth of Nations, Adam Smith stresses the role of Sentiment in market

exchange, e.g., trust. As Samuels

put it, “the order produced by markets can only arise if the legal and moral

framework is operating well” (Samuels

1977, 197). Together with division and specialization of labour, it

is market sentiments, according to Smith, that assures the wealth of nations.

In effect, Sentiment influences Reason and Reason influences Sentiment including

economic expectations. Put another way: no matter the price, would you buy a

used car from that person?

To the degree that various forms of capital –

cultural, financial, legal, physical and social – can be expressed as codified

and tooled knowledge, one may speak of ‘a knowledge theory of capital’. Such a theory is a corollary to a more general ‘labour

theory of knowledge’.

Labour (L)

In fact there are three forms

of Labour - Productive, Managerial & Entrepreneurial. All three forms embody personal knowledge.

Productive

Productive workers are those on the shop floor actually

producing goods & services. They are concerned with output. Their

knowledge is technical and specialized to a given industry or firm. In

effect they combine codified and tooled with personal & tacit knowledge

(memory and reflex) generally learned on the job in the Anglosphere.

Their knowledge involves making something or making something work. In

this sense the competitiveness of a firm or nation “depends not only on

sensible decisions about what to do, but on the availability of the

skills that are required to do it” (Loasby 1998, 143).

Managerial

Management, among other things, means “a governing body

of an organization or business, regarded collectively; the group of

employees which administers and controls a business or industry, as

opposed to the labour force”. It also means “the group of people who run

a theatre, concert hall, club, etc” (OED, management, n, 6). The role of

management is to make available the means (inputs) so that production

workers can perform their tasks and then to market and distribute the

output. In many ways management is like a choreographer, music or

theatre director. This sense of modern management is caught by Aldrich:

Thus the total operation is a performing art with

blueprints for score or choreography, the difference being that in this

technological case neither the co-ordinated performances (ballet) of the

skilled workers nor the finished product is put on exhibit simply to be

looked at, contemplated. It is a useful performing art. Its value is

instrumental.” (Aldrich 1969, 381-382)

Similarly, according to Schlicht, it is:

the fit of the organizational elements, rather than the

elements themselves, that characterizes a firm. Just as the quality of

an orchestra performance cannot be adequately measured by the average

quality of the performances achieved by the individual instruments, but

depends crucially on the way the instruments are played together, so the

productive value of a firm - as opposed to a set of individual

contracting relationships - emerges from the quality that has been

achieved through mutually adjusting the various activities that are

carried on. (Schlicht 1998, 208)

One crucial characteristic of the firm is custom

including tacit understandings of entitlements and obligations between

productive, managerial and entrepreneurial workers. This constitutes

part of what is commonly called ‘the corporate culture’ for which, on a

day-to-day.

Entrepreneurial

With the notable exception of

firms like Microsoft (Bill Gates) and Walmart (Sam Walton), most modern

corporations do not follow an original founder/owner but rather a ‘hired

gun’, or business entrepreneur. The word ‘entrepreneur’ comes from the

French entre meaning ‘between’ and prendre meaning ‘to

take’. The English ‘middleman’ retains this original sense.

During the Middle Ages and Renaissance, European traders (especially

from Venice and Genoa) ‘middled’, at high risk, between foreign

suppliers, e.g. of silk and spices from the Turks, and final consumers

in northern Europe. Today the term usually refers to someone who

sees and seizes an economic opportunity or a market opening or gap.

This may take the form of a new product or of servicing an existing

market in a new way. In both cases a high degree of creativity and

risk-taking is implicit. In this regard, the first English usage

of ‘entrepreneur’ was in 1828 meaning “the director or manager of a

public musical institution.” Today we would call this ‘an

impresario’. In fact, it was not until 1852 that entrepreneur took

its modern meaning of “one who undertakes an enterprise; one who owns

and manages a business; a person who takes the risk of profit or loss

(OED, entrepreneur, a, b).

Entrepreneurial knowledge is

intuitive in seeing and taking advantage of invariants and affordances

in a market that others do not see. It involves seeing and

realizing a vision of future markets, products and opportunities.

Ignorance is the opposite of knowledge, i.e., want of knowledge.

The non-rational way of entrepreneurial vision was called ‘animal

spirits’ by Keynes (Keynes 1936, 161). Like some ancient

priest-king, the entrepreneur ‘knows’ the future and leads his people

(investors, managers, workers and consumers) into it – right or wrong -

to success or failure. In a manner of speaking, prophets today

seek profits, not souls. Ideally, this highly valued form of

pattern recognition works best as “informed intuition” (Jantsch 1975).

All available information, knowledge and opinion is explicated but then

an intuitive, inductive judgmental vision is conjured up. In a sense,

the business entrepreneur or CEO has assumed the mantle of the Western

Cult of the Genius joining the artist, inventor and scientist.

Natural Resources (N)

Similarly, the definition of what

constitutes a natural resources is constantly evolving.

At first

glance, natural resources have no relationship to knowledge. By

definition, they exist as John Locke said in “the State that

Nature hath provided” (quoted in

Dooley 2002,

4). They are just part of the environment until the knowing mind

recognizes them as useful. Thus oil lay in the ground virtually

untapped until invention of the internal combustion engine. Just

as we recognize a tool by its purpose (M. Polanyi 1962, 56), we

similarly identify natural resources by the human ends we

attribute to them. At a given point in time a naturally

occurring substance is seen as nothing but an environmental

feature. Take a pathway through the jungle one day and you see a

large rock outcrop. The next day, with new knowledge, the same

path leads not to an environmental feature but to a bauxite

deposit that can be converted into aluminum. It has become a

toolable natural resource. Yet it itself has not changed, one

day to the next, rather new knowledge allows us to see it in a

different light. This ‘changed way of

seeing’ is captured by Loasby when he writes:

Menger begins

by arguing that an object becomes a good only when someone

discovers how to use it to satisfy some human need. Goods are

endogenous, created by new connections between human need and

physical or human resources; and their value is derived from the

need which each of them serves and - crucially for this paper -

from the knowledge that it can serve this need and also the

knowledge of how it can be made to do so… The creation of goods,

and of technology, rests on the creation of knowledge, and

therefore on previous uncertainty - or indeed sheer ignorance.”

(Loasby

2002, 6)

Today the most striking example of how new knowledge

transforms environmental features into toolable natural

resources is biotechnology. While advances in analysis

and sequencing now allow researchers (and hence firms) to

experiment with known genetic command codes to build new

drugs, enzymes, pathways, proteins et al, the reality

is that the raw material for biotechnology is life itself –

everywhere and every when. Nature is much older and more

experienced in designing command codes under a wide range of

environmental conditions than emergent biotechnology.

Accordingly Nature has become the object of search by the

biotech industry for

novel code.

This search is called ‘bioprospecting’ and takes two forms:

ethnobiology and ‘original research’ which is

self-explanatory.

Ethnobiology is the interdisciplinary study of how human

societies use or have used flora and fauna to serve human

purpose, e.g., for medical or nutritional purposes.

Its principal sub-disciplines include ethnobotany,

ethnomycology, ethnolichenology, ethnozoology, ethnoecology,

paleoethnobotany, and zooarchaeology. The

Society of Ethnobiology

publishes a journal documenting activities in these fields.

Non-linked references

Blaug, M.,Economic theory in retrospect, Cambridge

University Press, 5th Edition, 1996

Jantsch, E. Design for Evolution, Braziller, NY,

1975.

Observation #4:

Technological Change

What do we mean by technology?

The word ‘technology’ entered the English language only in

1859 according to the Merriam Webster Dictionary

deriving from the Greek techne meaning Art and

logos meaning Reason, i.e., reasoned art. The

Oxford English Dictionary (OED, technology, 1 b) reports

it was re-coined at that time by Sir Richard Francis Burton,

Victorian explorer and translator of the Kama Sutra

(1883), the Arabian Nights (1885) and the Perfumed

Garden (1886).

It was Karl Marx, however,

(1818-1883) who produced the first true philosophy of

technology combining ‘the means of production’ with a

humanist critique rather than simple glorification of

Victorian progress. It is important to realize that the

technological imperative drives Marxian analysis. Class

warfare is collateral damage. This Marxian connection

tainted reception of all subsequent philosophies of

technology in the English-speaking world or Anglosphere.

Arguably, it was the work of Martin Heidegger (a purported

Nazi sympathizer) specifically his 1954 essay ‘The

Question Concerning Technology’ that finally led,

in 1983, to founding the American Society for Philosophy and

Technology (Idhe

1991, 4). Please see the journal,

Techne. Physical technology, to paraphrase

Heidegger, is the enframing and enabling of Nature to serve

human purpose.

In Economics, measurable

technological change only entered the mainstream in 1957

when economist Robert Solow published "Technical

Change and the Aggregate Production Function". In it he presented what is known as

the Solow Residual. It begins with a symbolic

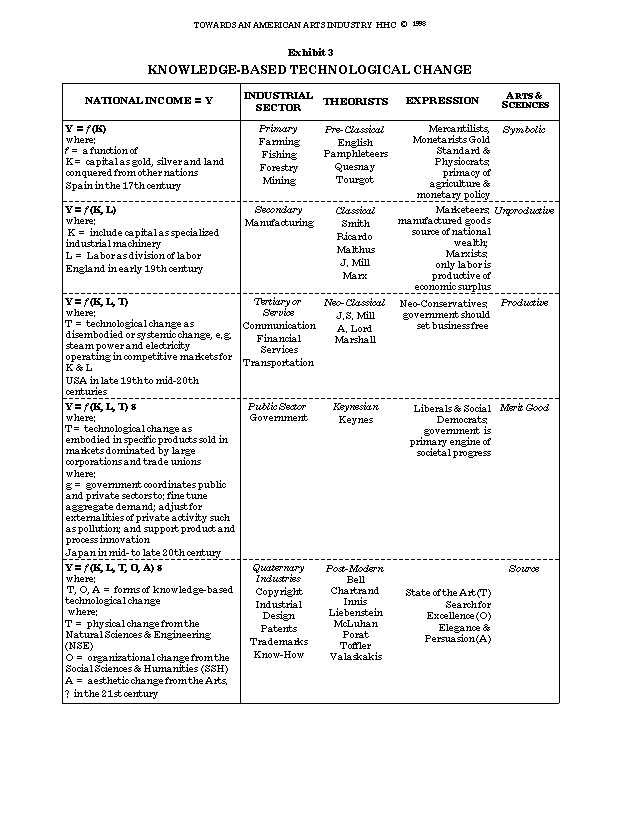

equation for the production function: Y = f (K, L, T)

which reads: national income (Y) is some function (f)

of capital (K), labour (L) and technological change (T).

Subsequently, in 1962, Solow

introduced the concept of 'embodied technological change' in “Technical Progress,

Capital Formation and Economic Growth”. Embodied

technological change refers to

new technology fitted into

actual products

like the transistor in the

transistor radio. By contrast disembodied

technological change tends to spread evenly across an

economy such as improvements in communications and

transportation or what the Victorians would have

called 'Progress'. In addition there is endogenous and

exogenous technological change, i.e., change

resulting from economic imperatives (endogenous to the

economic system) and changes resulting from the work of

independent scientists, inventors and other creators

(exogenous

to the economic system).

Technological change in the

Standard Model of Market Economics refers to the impact of

new knowledge on the production function of a firm or

nation. The content and source of that knowledge is

not a theoretical concern; what matters is its mathematical

impact on the production function. Over the last

hundred years, depending on the study, something like 25% of

growth in national income is measurably attributable to

changes in the quantity and quality of Capital and Labour

while 75% is the residual Solow attributed to technological

change. Yet we have no idea of why some things are invented

and others not; and, why some things are successfully

innovated and brought to market and others are not.

The Solow Residual is known in the profession as the

measure of our economic ignorance. The economic

effects of this residual was called 'creative destruction'

by economist Joseph Schumpeter. The

'residual' is why I became an economist distinguishing,

during my career, between Physical Technology (P) emerging from the

Natural & Engineering Sciences; Organizational Technology

(O)

emerging from the Humanities & Social Sciences; and, Design

Technology (D) emerging from the Arts or what I call the POD

Model of Technological Change.

For more information please see

my:

Creative Destruction: The Economic Meaning of Technological

Change, especially

Exhibit 1: Evolution of the Production Function.

All cost considerations involved in internalizing a process can be

overturned due to changes in technology, e.g., information technology in the 1980s reduced the need for middle management

and resulted in significant 'downsizing' of large firms.

As has been demonstrated, however, new

knowledge has many sources and varying effects. It may be productive,

increasing output on the shop floor; it may be managerial reducing costs or

increasing sales; or, it may be entrepreneurial realizing a vision of future

markets, products and/or other opportunities. It may flow from the natural and

engineering sciences (physical technology), the humanities and social sciences

(organizational technology) or the Arts (design technology). In economic

theory, however, it does not matter what form new knowledge takes; it does not

matter from whence it comes; the only thing that matters, in terms of calculatory rationalism, is its mathematical impact on the production function.

In response to technological change, the production function for

output may shift upwards or downwards, i.e., technology can be lost as

happened with the fall of Rome. The quantity and/or cost per unit output may

increase or decrease. Alternatively, an entirely new production function may

emerge with innovation of new and/or elimination of old products, processes and

techniques. Technological knowledge does not only accumulate; it also withers

away if not transmitted to subsequent generations. The later is most apparent

with respect to traditional craft methods (White & Hart 1990). The process has

been compared by Kaufmann to speciation and extinction in biology (Kauffman

2000 216).

In the 20th century, technological change became recognized as

the most important source of economic growth, i.e., increase in output –

absolutely, or, per capita. Our understanding of such change, however,

remains limited. We do not understand why some things are invented and others

are not; why some are successfully innovated and brought to market, and others

are not. The contribution of technological change has, in theory, traditionally

been treated as a ‘residual’, i.e., after measuring total growth of

output, the contribution of an increased quantity and quality of capital, labour

and natural resources are factored out and the residual is called technological

change. Again, technological change, in this sense, is a residual amounting to an

error term, or, a measure of our economic ignorance. In this regard,

Kaufmann criticizes the Standard Model and suggests such

‘ignorance’ can be resolved using the concept of coevolution and coconstruction

(Kauffman

2000, 222).

Non-linked references

White, B. & Hart A-M, (eds), Living Traditions

in Art: First International Symposium, Dept. of Education in the

Arts, Faculty of Education, McGill University, Montreal, 1990.

Observation #5:

Fiscal Policy in Canada

i - Purpose

ii -

Assumptions

iii - Ground

Rules

iv - Putting the Question

v -

Terminology

vi - Process & Problems in Canada

i - Purposes

Until

the Keynesian Revolution of the 1930’s (put into motion by the

political impact of the Great Depression), the almost exclusive fiscal

concern of Government in ‘liberal democracies’ of the West was

financing and fulfilling ‘political’ objectives – domestic and

geopolitical. Overall, or ‘macroeconomic’ performance was a given,

not an end or objective to be pursued. The market would

‘self-adjust’ and Government would hold on as ‘bust’ turned into

‘boom’ and then into ‘bust’ again riding the tail of the dragon.

People would suffer or prosper according to the timing and dictates of

market prices with little if any assistance from Government

The Classical and Neo-Classical Periods of economic

history thus reversed Mercantilism that had preceded them. From an

economy as a Crown Privilege to be used, regulated and controlled by the

whim and passion of a moody Prince, the economy became forbidden

territory into which a democratic, liberal government dare not tread. In

summary, the progress of Classical and Neoclassical Political Economy

was the withdrawal of the State from the economy with the notable

exception at the beginning of the 20th century of anti-trust or

anti-combines policy – breaking up trusts and monopolies that, like

Government itself, could corrupt perfect competition and foreclose a

‘just price’ in individual markets. As for the economy as a whole,

the rationale was governmental non-interference.

An important political boost to this rationale was

provided by the rise of socialist and communist political power. With

the defeat of Napoleon III in 1870 by Germany, civil war broke out in

France between liberal democrats (Republicans) and the Paris Commune

(Communists). Socialist and communist thought argued that the answer to

the arbitrariness of both Princes and Prices was total public

ownership of the economy in the name of the people. Paris burned and

laissez-faire capitalism, more or less, triumphed. France remains,

however, much more prone to Government economic interference than

Anglo-American cultures. This fear of public ownership was re-ignited

and then made real with the Russian Revolution of 1917 and the

subsequent Civil War ending 1921 with ‘Communist’ victory.

In 1944 Karl Polanyi, brother of the chemist and philosopher of science,

Michael Polanyi, published the first edition of The Great

Transformation. It treats the rise of the self-regulating market and

the decline of traditional social institutions. According to some

scholars this book is of renewed relevance in a post-Cold War world due

to the emergence of a global knowledge-based economy (Block

2001;

Munck 2002).

Since Keynes, however, macroeconomic performance

(including economic growth and price stability) has become an essential,

if still secondary, policy objective of the modern State. The business

cycle has, to a degree, been usurped by a public policy cycle. Enormous

deficit spending during the 1960’s through 1970s was followed by

increasingly strict ‘deficit and debt’ reduction, downsizing of the

public sector during the 1980s and 1990s with ‘surplus’ spending

beginning a new public policy phase in the early 2000s

to burn out in the Great Recession of 2008, also known as the Long

Recession. Austerity - deficit and debt - was the response of

governments around the world. In many ways repeating the mistakes

of the past - the Great Depression. Like the 1930s initial

stimulus was followed by austerity. This time, however, monetary

authorities intervened softening but not reversing the decline with

experiments like quantitative easy of which more later.

It can, however, be argued that the hard lessons learned

in the 1930s were not forgotten even at the height of the

‘neo-conservative’ (so-called in the English speaking world) or

‘neo-liberal' (so-called in France and most of continental Europe)

political movement of the 1980s and early to late 1990s. The ship of

state continued its course towards a ‘welfare state’ in which

Government has a legitimate role to play in the social and economic

development of the nation (see:

Government

by Moonlight). The difference is that many functions assumed by

Government between the 1930s and 1970s have been downloaded to smaller

‘private’ or semi-private vessels. Overall culture, education,

employment, the environment, health care and welfare (or ‘workfare’)

of society and its members as well as economic growth and price

stability remain responsibilities of the post-modern Nation State. Such

responsibilities are, if anything, taking on even greater importance as

‘competitive factors’ in the emerging global economy emerges. The

only questions remaining are: who should deliver such services –

Government, the profit or the nonprofit sector and how should delivery

be monitored? The services, however, must be delivered in an equitable

manner with citizens protected by a ‘social safety net’ that varies

between States but is present, nonetheless, in all, even the most

capitalist – the United States of America.

One of the ironies accompanying the ascendance of

macroeconomic objectives by politically elected Government is that until

the 1970s most universities in North America, and the English-speaking

world in general, did not have ‘departments of economics’. Rather,

the more usual disciplinary designation was “political economics”.

But just as the legitimacy of Government’s role in macroeconomics

affairs reached a zenith not seen since the Mercantilist Period of

economic history, such departments split into separate and distinct

Departments of Economics and Political Science.

The fiscal policy process is as much cultural as

economic, that is, it is a cultural economic phenomenon. The USA

budgeting process (dominated by the legislative branch) is very

different from that of Canada that is different from the United Kingdom

(both dominated by the Executive Branch) that is different from France

that is different from Germany, etc. Each country even has its own

distinct rituals and traditions associated with the fiscal policy

process. For example, in Canada the Minister of Finance is expected to

wear a pair of new shoes while in Britain the Chancellor of the

Exchequer is to use an old beaten up briefcase to present the budget to

the British House of Commons. Accordingly, what follows applies

only in Canada. It is extracted from my longer paper:

A

Radical Analysis of 'Personal' Taxation.

ii - Assumptions

I

begin with five assumptions about the Canadian budgetary purpose. First,

there are two sides to the coin of fiscal policy – pleasure and pain.

The pleasure (including relief from pain) flows from spending public

monies – fiscal policy. Pain flows from collecting private

monies to pay for public spending – tax policy. Like carrot and stick,

a democratic government-of-the-day uses public finance to adjust, adapt

and evolve society and the economy towards its ‘ideological’ goals

and objectives that extend above and beyond macroeconomic growth and

price stability.

Second, the only way

to gain more pleasure without more pain is through a growing economy.

In the long run, however, a growing economy can be maintained only if

public finance does not “kill the goose that lays the golden egg”.

Third, rational

citizens will do their best – in or out of a growing economy - to

minimize their pain and maximize their pleasure through lobbying,

protests and voting.

Fourth, in their

annual budgets, federal, provincial and local governments flip the coin

seeking a politically workable, socially desirable, balance between the

‘heads-I-win’ and ‘tails-you-lose’ of public finance.

Fifth,

the game of public finance is worth playing, at a minimum, because of

‘market failure’, that is:

·

there are some

goods and services (public goods) essential to modern life that cannot

be produced by the private sector, e.g. municipal bridges and roads,

compulsory mass education, contagious disease immunization, national

defense, etc.; and,

·

perfect

competition is not common in the ‘real world’. Usually some players

in the economy (typically a small group or oligopoly) exercise market

power over the price and quantity of goods and services available to

consumers. The existence of such ‘market power’ justifies a public

response including spending, e.g. funding anti-combines agencies, and,

taxation.

iii - Ground Rules

Beyond

the constitutional reality that public finance is conducted in the name

of Her Majesty in right of Canada and in Her right of each of the ten

Provinces, there are five ‘ground rules’ for this annual coin toss:

a) the Constitution establishes, in broad terms - subject to varying

interpretation:

·

on what federal and

provincial governments can spend;

·

by what means they can

raise public monies; and, · in subordinating local to provincial

government;

b)

three legal systems interactively define persons, property and taxation

in Canada:

·

criminal law, the

prerogative of the federal government but with administration shared by

the Provinces;

·

civil law, essentially

the responsibility of the Provinces with Quebec being the extreme case

governed by a variation of the European Civil Code rather than

Anglo-American Common Law as in other Provinces, e.g. torts

(non-contractual damages) based on precedent (Common Law) rather than

principle (Civil Code); and,

·

tax law, a shared

responsibility of the federal and provincial governments;

c) the federal government ‘owns’ the coin through

the Bank of Canada and influences its value through exclusive control of

monetary policy;

d) the federal government can define and redefine what

are legitimate sources of public monies, e.g. income tax introduced

during WWI as a ‘temporary’ war measures act, and, the 1970

amendment to the Criminal Code permitting lotteries (gaming in general

including ‘video lottery terminals’ or slot machines) to become an

increasingly significant source of public monies for the Provinces; and,

e)

the federal government indirectly influences settlement of public

finance disputes with citizens and the Provinces through its prerogative

of appointment to the Federal (formerly the Exchequer Court) and the

Supreme Courts of Canada.

iv - Putting the Question

Subject

to these ground rules, each senior level of government (federal and

provincial governments) annually put the following ‘pleasure’

questions to the people:

·

who or what will enjoy

public funding: the poor and needy; the average citizen; the corporate

citizen; city or rural dwellers; foreigners, i.e. foreign aid; and/or,

abstract policy categories such as education, the environment, health

care, protection of persons and property, etc;

·

what pleasures will they

enjoy, e.g. direct dollars in the pocket (grants in aid), civil service

employment, public infrastructure and essential services, investment

and/or loans in support of private and/or semi-private ventures, and/or

relief from taxation e.g. tax expenditures including refundable and

non-refundable tax credits;

·

how much pleasure will be

allowed, e.g. marginal or significant to the life of citizens –

corporate or individual; and,

·

when will the pleasure be

provided, e.g. weekly, monthly, quarterly, annually?

Similarly,

each government annually puts the following questions about the pain of

public finance - direct and indirect, ‘near’ and ‘voluntary’

taxes - to the people:

·

who will suffer so they

and/or others may ultimately enjoy the pleasures of public spending;

·

what forms of pain must

citizens endure, e.g. corporate, excise, income, near taxes (e.g.

fees-for-service), sales and/or voluntary (e.g. lotteries) taxes;

·

how much pain from any

one and/or all taxes - should one person or any ‘class’ of taxpayers

bare (tax burden);

·

when and by what means should they suffer, e.g., monthly,

point-of-sale, quarterly and/or withholding-at-source; and,

·

at what threshold should the quality and/or quantity of pain

change or stop, i.e. what are the tax brackets?

v - Terminology

Fiscal

policy or ‘public finance’ involves primary political choices, each with its

associated opportunity costs. Fiscal

policy involves answering hard questions about what pleasures to publicly

provide, to whom, how much, and, how to inflict the pain necessary to raise the

required public funds. Attaining

macroeconomic objectives like fostering economic growth and maintaining price

stability provide only a ‘glass ceiling’ above the heated political debate

of making the ‘tax and spend’ choices of each and every Government.

The ceiling, however, has a great deal of flexibility.

The Keynesian Revolution called for spending in bad times and saving in

good times. This is not what

Government did.

From

the 1960s to the mid-1990’s Government around the developed world spent in

good and bad times. In fact, they spent more than they willing to pay in

additional pain to the taxpaying public. So

they ‘borrowed’. Politics

thereby raised the ceiling. The

ceiling only began to come down when ‘deficit and debt’ became the political

mantra of the industrial world and interest payments on the national debt the

largest single and least satisfying pleasure paid for out of the public purse.

By

the late 1990s, deficits were slashed; debt began to shrink; and, social

infrastructure built up over two generations crumbled but fortunately did not

collapse. As the 21st

century begins, the word ‘surplus’ has even re-entered the political

vocabulary. Inevitably,

perhaps, the heat generated by all the public policy spheres rubbing up against

each other is threatening to raise the ceiling once again.

Jockeying to be first to fill its specific ‘deficit’ incurred during

the ‘slash and cut’ of public debt and deficit reduction, each public policy

sphere is raising its profile before the political public.

Collectively, their wants, needs and desires threaten macroeconomic goals

such as economic growth (increasing potential real GDP) and price stability (low

inflation). If the GDP pie grows

and the cost of its slices does not increase then more public pleasure may be

had with no increase in public pain in the form of taxes or interest payments on

the national debt. If not, some

will win and some will lose. It is

to the naming of these various Canadian spheres of political influence that now

I turn.

As

a federation, Canada has had amply time to sort out the naming of these spheres

of public policy. Since at least 1918 with the founding of the Dominion Bureau

of Statistics (now Statistics Canada), the federal and provincial governments

have come to agreement on certain terms. These

became embodied in The Canadian System of Government Financial

Management Statistics (CSGFMS). In 2001 the system became a

victim of globalization and a general decline in the quality of the publicly

generated statistical evidence. One thing is certain, it will take decades

to develop actionable time series.

The FMS

was founded on a modified-cash based system of accounting. Recently,

Canadian governments have decided to move from that modified-cash based

accounting system to an accrual based accounting system. In addition, an

internationally accepted Government Finance Statistics (GFS) manual has

been developed. The GFS

2001 is an internationally accepted accrual accounting framework for

government finance statistics. The

GFS 2001 is also

fully integrated with the United Nations (UN) System of National

Accounts (SNA) framework. Given these changes, the Canadian statistical

system underlying government finance statistics must also change.

Statistics Canada has decided to move towards reporting government

finance statistics on a Government Finance Statistics 2001 (GFS

2001) basis.

In the following I will deal with the original

'made-in-Canada' system. The

CSGFMS was used for purposes of the Fiscal Arrangement Act between the

federal and provincial governments. The CSGFMS was used to calculate, among other things,

equalization payments by the federal government to the ‘have-not’ provinces

of the country. Next to the System

of National Accounts (to which it is fully compatible), the CSGFMS was the most important system of economic statistics in Canada.

For

purposes of illustration please find below top-level CSGFMS terms used for: a)

assets & liabilities of government in Canada; and, b) revenue and c)