|

Supply refers to the

willingness of producers to provide a given quantity of output at a

given price. Such willingness reflects the production function of

each firm inclusive of technology, the cost of inputs and the

revenue received for its output. All things being equal ‘The Law of

Supply’ is operative, i.e., the higher the price the greater

the supply, the lower the price, lower the supply. There is

therefore an upward sloping supply curve. Why? As we will see: the

Law of Diminishing Marginal Product.

The

Firm

In Industrial Organization,

the firm is located in four dimensions. First, buyers and

sellers exchange of goods and services in markets – geographic,

commodity-based and/or virtual, e.g., Ebay. Second, a

firm or enterprise is any entity engaging in productive activity -

with or without the expectation of profit. This includes profit,

nonprofit and public enterprise as well as self-employed

individuals. All enterprises have scarce resources and are

accountable to shareholders and/or the public and the courts. A

firm or enterprise is defined in terms of total assets and

operations controlled by a single management empowered by a common

ownership. Third, an industry is a group of sellers of

close-substitutes to a common group of buyers, e.g. the

automobile industry. Fourth, a sector is a group of related

industries, e.g. the automobile, airline and railway

industries form part of the transportation sector. Often ‘sector’

and ‘industry’ are used interchangeably, for example - the

biotechnology industry or sector.

In the standard model of

market economics, a.k.a., Microeconomics, a firm is a

technical unit engaged in the production of one or a group of very

closely related commodities. In theory, it is a single product firm

with the entrepreneur as a surrogate for a decision-making

hierarchy. It is the study mainly of external behavior and internal

cost analysis, i.e. it not about business management.

Furthermore, profit maximization is the only goal of the firm.

Production Function

In symbolic logic the

production function of

a firm is:

(7) Q = g (K, L, N)

where:

Q = output

g

= some function reflecting ‘know-how’ in combining factors to

produce into outputs

K = capital

L = labour

N = natural resources that

can be enframed and enabled to serve human purpose.

The production function is time sensitive.

However, the short- and long-run in economics is measured not in

chronological time but in functional time, e.g., how long it

takes to build a new plant. Thus the long-run in the restaurant

industry is chronologically shorter than in the steel or nuclear

industries but both are functionally the long-run in their

respective industries. There are three types of time periods. To

graph in two dimensional space only K and L are considered.

Very Short-Run

In the very short run, or what Marshall called

‘the market period’, output is fixed. All factors of production are

fixed – labour, capital and natural resources. The very short-run

supply curve is vertical and does not change with price. An example

is the farmers’ market where produce is brought into the city from

the farm for sale. No more produce is available. What is on hand

is all that can be sold, no matter price.

(8) Q = g (K, L)

where

K, L & Q are all fixed

Short-Run

In the short-run at least one factor of

production is fixed, generally capital plant and equipment. More or

less labour and natural resources can be employed and output

increased or decreased.

(9) Q = g (K, L)

where

K is fixed

L is variable

Q is variable

With capital fixed and labour

variable in the short run we can graph the production function as an

'S' shaped curve. Initially as labour is added its

marginal product increases up to about 2.5 units in the graph

(increasing MPL) and then it begins to decrease from 2.5

up to 6.5 units (diminishing MPL) becoming zero at the

peak of the curve and then turns negative (negative MPL).

No profit maximizing firm will expand by hiring more labour if total

output is decreased, i.e., beyond the peak of the production

curve. There are, of course, some firms such as

State owned companies in China that are not profit maximizers but

rather employment maximizers.

Why does MPL eventually decline and become negative.

The simple answer is that capital is being spread thinner and

thinner among more and more workers reducing their marginal product.

In addition more and more workers means increased congestion and

complexity. This is called the law of eventually diminishing product

which has significant implications for the costs of a firm as output

rises. It parallels the law of eventually diminishing

utility in Consumer Theory, i.e., eventually the marginal

utility of a good declines and becomes negative, too much of a good

thing makes you sick. The marginal product of labour, i.e., the

additional output generated by employing one more unit of labour is

measured by the slope of the production function. The average

product of labour, or the average output of all workers, is measured

by the slope of a ray, i.e., straight line, from the origin

where it intersects the production function. It should be

noted that some rays will intersect the production function at two

points. At each of these two points marginal product is the

same. As will be seen this has significant implications for

the shape of the marginal and variable costs curves of a firm,

specifically their 'U' shape. As will be seen, if we know the

cost of labour we can calculate the marginal cost of an additional

unit of output and the average variable cost of any given level of

output.

Long-Run

In the long-run all factors of production are

variable – capital plant & equipment, labour and natural resources.

(10) Q = g (K, L)

where

K is variable

L is variable

Q is variable

As noted previously modern

microeconomic theory began with demand and the constrained

maximization of utility by the consumer demonstrated using

indifference curves and budget constraint. Initial attempts to

explain production adopted the same basic mechanism with one

important change: measurement of output is cardinal. That is we

can, unlike utiles, count the exact number of units being produced.

The firm thus wants to maximize output

(Q):

(11) Q = g (K, L)

The firm, however, faces a constraint: the cost

of inputs or factors of production. In symbolic logic, this cost

constraint is:

(12) C = PKK + PLL

where

K = capital

L = labour

PK = price of

capital

PL = price of

labour

Assuming all factors are infinitely divisible

then different levels of Q can be produced using different factor

combinations. This generates an isoquant a curve representing a

constant level of output all along its run (R&L

8A-1; M&Y 10th

Fig. 8.2). The slope

of the isoquant is the marginal rate of technical substitution (MRTS)

of capital for labour maintaining the same Q. In symbolic logic it

is

(13) MRTS = MPK/MPL where

MPK = marginal product of capital

MPL = marginal product of labour

There are theoretically an infinite number of

isoquants rising to higher and higher levels of output (R&L

8A-2). They are

convex to the origin (opening away) due to the Law of Diminishing

Marginal Product which states that as one factor is given up in favour of another eventually marginal product of the increasing

factor will decrease.

While the firm wants to maximize Q it faces a

cost constraint. For a given cost a maximum amount of capital or

labour can be bought illustrated by the intercepts of the x- and

y-axis. Its slope is the relative cost of the two factors or in

symbolic logic is:

(14) Cost Ratio = CL/CK

As with the budget constraint price ratio by

convention the cost ratio is the inverse of the slope of the

resulting cost constraint curve. The curve shows all combinations

of K and L that can be bought for a specific cost (R&L

8A-3; M&Y 10th

Fig. 8.2). Maximum Q

for a specific cost is achieved where the cost constraint just

touches or is tangent to the highest attainable isoquant. At that

point, the slope of the cost constraint equals the slope or MRTS of

the isoquant.

(15)

MRTS = MPK/MPL

= 1/(CL/CK)

and

(16) MPK/CK

= MPL/CL where

dollar-for dollar the

marginal product of an additional unit of L is equal

dollar-for-dollar to the marginal product of an additional unit of K

Expansion Path

As with consumption and the Income Consumption

Curve, if we relax the cost constraint while holding factor prices

constant, a new cost constraint with the same slope (1/CL/CK)

is created and a new equilibrium established. Repeating this

process a locus of point is created all of which satisfy the

equilibrium conditions (MPK/CK

= MPL/CL) forming the expansion path

for the firm (M&Y

10th

Fig. 8.18).

This initial attempt to plot the supply curve of

the firm was judged inadequate for the simple reason that factors of

production especially capital are not infinitely divisible but

rather ‘lumpy’ particularly in the short-run. A new approach was

required that focused on the short-run behavior of the firm.

Factors of Production

Before considering how to derive the supply curve of a firm it is

appropriate to consider the inputs to the process. Factors of

production or inputs are the ingredients used by a firm to produce a

good or commodity. Traditionally there are three capital, labour

and natural resources. Their meaning has, however, evolved over

time. My summary of the evolution of the production function

follows description of factors of production as

Exhibit 1 (below).

Capital

The concept of capital has mutated and expanded through the history

of capitalism. To the Mercantilists of the 17th century, capital

was gold, silver, land and slaves. To the Physiocrats of

pre-Revolutionary France, it was the surplus generated by

agriculture. To the Classical School of the late 18th and early

19th centuries, it was the surplus resulting from specialized

physical plant and equipment combined with the division and

specialization of labour. To the Neo-Classical School of the late

19th and 20th centuries, it was financial capital. To Bohm-Baverk

and the Austrian School, capital was historically embodied labour

produced through ‘round-about’ means of production (Blaug 1968,

510-11). How to measure such embodied labour has never, however,

been satisfactorily answered (Dooley 2002). Today, when economists

speak of capital, they may refer to cultural, financial, human,

legal, physical, social or other forms expressed as a stock existing

at a given moment in time. For our purposes, however, capital is

restricted to physical plant and equipment and its equivalent

financial value.

Labour

Labour, unlike capital, has been subject to definitional reduction

rather than expansion. It has been subject to capitalization rather

than humanization as a factor of production. Thus education and

training add to the stock of ‘human capital’, something

ideologically alienated from labour and subject to managerial

control as a corporate or national asset. Similarly,

entrepreneurship and management have become detached from labour

even though separation of ownership from control – public or private

- makes the manager an employee or agent, not a principal or owner.

In effect, labour becomes warm hot bodies applying muscle not brains

doing what it is told. Effort is organized according to a division

and specialization of labour (brawn) determined by a specialized

class of employee called management (brains). In fact there are

three forms of Labour - (i) Productive, (ii) Managerial & (iii)

Entrepreneurial.

(i) Productive

Productive workers are those on the shop floor actually producing

goods & services. They are concerned with output. Their knowledge is

technical and specialized to a given industry or firm. In effect

they combine codified and tooled with personal knowledge (memory and

reflex) generally learned on the job in the Anglosphere. Their

knowledge involves making something or making something work. In

this sense the competitiveness of a firm or nation “depends not only

on sensible decisions about what to do, but on the availability of

the skills that are required to do it” (Loasby 1998, 143).

(ii) Managerial

Management, among other things, means “a governing body of an

organization or business, regarded collectively; the group of

employees which administers and controls a business or industry, as

opposed to the labour force”. It also means “the group of people who

run a theatre, concert hall, club, etc” (OED, management, n, 6). The

role of management is to make available the means (inputs) so that

production workers can perform their tasks and then to market and

distribute the output. In many ways management is like a

choreographer, music or theatre director. This sense of modern

management is caught by Aldrich:

Thus the total operation is a performing art with blueprints for

score or choreography, the difference being that in this

technological case neither the co-ordinated performances (ballet) of

the skilled workers nor the finished product is put on exhibit

simply to be looked at, contemplated. It is a useful performing art.

Its value is instrumental.” (Aldrich 1969, 381-382)

Similarly, according to Schlicht, it is:

the fit of the organizational

elements, rather than the elements themselves, that characterizes a

firm. Just as the quality of an orchestra performance cannot be

adequately measured by the average quality of the performances

achieved by the individual instruments, but depends crucially on the

way the instruments are played together, so the productive value of

a firm - as opposed to a set of individual contracting relationships

- emerges from the quality that has been achieved through mutually

adjusting the various activities that are carried on. (Schlicht

1998, 208)

One crucial characteristic of the firm is custom including tacit

understandings of entitlements and obligations between productive,

managerial and entrepreneurial workers. This constitutes part of

what is commonly called ‘the corporate culture’ for which, on a

day-to-day.

(iii) Entrepreneurial

With the notable exception of firms like Microsoft (Bill Gates) and

Walmart (Sam Walton), most modern corporations do not follow an

original founder/owner but rather a ‘hired gun’, or business

entrepreneur. The word ‘entrepreneur’ comes from the French entre

meaning ‘between’ and prendre meaning ‘to take’. The English

‘middleman’ retains this original sense. During the Middle Ages and

Renaissance, European traders (especially from Venice and Genoa) ‘middled’,

at high risk, between foreign suppliers, e.g. of silk and spices

from the Turks, and final consumers in northern Europe. Today the

term usually refers to someone who sees and seizes an economic

opportunity or a market opening or gap. This may take the form of a

new product or of servicing an existing market in a new way. In

both cases a high degree of creativity and risk-taking is implicit.

In this regard, the first English usage of ‘entrepreneur’ was in

1828 meaning “the director or manager of a public musical

institution.” Today we would call this ‘an impresario’. In fact,

it was not until 1852 that entrepreneur took its modern meaning of

“one who undertakes an enterprise; one who owns and manages a

business; a person who takes the risk of profit or loss (OED,

entrepreneur, a, b).

Entrepreneurial knowledge is intuitive in seeing and taking

advantage of invariants and affordances in a market that others do

not see. It involves seeing and realizing a vision of future

markets, products and opportunities. Ignorance is the opposite of

knowledge, i.e., want of knowledge. The non-rational way of

entrepreneurial vision was called ‘animal spirits’ by Keynes (Keynes

1936, 161). Like some ancient priest-king, the entrepreneur ‘knows’

the future and leads his people (investors, managers, workers and

consumers) into it – right or wrong - to success or failure. In a

manner of speaking, prophets today seek profits, not souls.

Ideally, this highly valued form of pattern recognition works best

as “informed intuition” (Jantsch 1975). All available information,

knowledge and opinion is explicated but then an intuitive, inductive

judgmental vision is conjured up. In a sense, the business

entrepreneur or CEO has assumed the mantle of the Western Cult of

the Genius joining the artist, inventor and scientist.

Natural Resources

At first glance, natural resources have no

relationship to knowledge. By definition, they exist as John Locke

said in “the State that Nature hath provided” (quoted in

Dooley 2002, 4). They are just part of the environment until the

knowing mind recognizes them as useful. Thus oil lay in the ground

virtually untapped until invention of the internal combustion

engine. Just as we recognize a tool by its purpose (M.

Polanyi 1962, 56), we similarly identify natural

resources by the human ends we attribute to them. At a given point

in time a naturally occurring substance is seen as nothing but an

environmental feature. Take a pathway through the jungle one day

and you see a large rock outcrop. The next day, with new knowledge,

the same path leads not to an environmental feature but to a bauxite

deposit that can be converted into aluminum. It has become a

toolable natural resource. Yet it itself has not changed, one day

to the next, rather new knowledge allows us to see it in a different

light. This ‘changed way of seeing’ is captured by Loasby when he

writes:

Menger begins by

arguing that an object becomes a good only when someone discovers

how to use it to satisfy some human need. Goods are endogenous,

created by new connections between human need and physical or human

resources; and their value is derived from the need which each of

them serves and - crucially for this paper - from the knowledge that

it can serve this need and also the knowledge of how it can be made

to do so… The creation of goods, and of technology, rests on the

creation of knowledge, and therefore on previous uncertainty - or

indeed sheer ignorance.” (Loasby 2002, 6)

Today the most striking example of how new

knowledge transforms environmental features into toolable natural

resources is biotechnology. While advances in analysis and

sequencing now allow researchers (and hence firms) to experiment

with known genetic command codes to build new drugs, enzymes,

pathways, proteins et al, the reality is that the raw material for

biotechnology is life itself – everywhere and every when. Nature is

much older and more experienced in designing command codes under a

wide range of environmental conditions than emergent biotechnology.

Accordingly Nature has become the object of search by the biotech

industry for novel code. This search is called ‘bioprospecting’ and

takes two forms: ethnobiology and ‘original research’ which is

self-explanatory. For our purposes, however, we will restrict

factors of production to capital and labour.

Exhibit 1

Evolution of the Production Function

|

Exemplar Economy |

Sector |

Production Function |

Accreting Factors of

Production |

|

Spain

16th, 17th

to mid-18th centuries |

Primary

farming, fishing,

forestry & mining |

Y = f (K) |

K =

gold, silver, land &

slave labour |

|

England

late 18th to

mid-19th centuries |

Secondary

manufacturing |

Y = f (K, L) |

K = manufacturing plant

& equipment

L = division &

specialization of free labourers |

|

U.S.A.

late 19th to

mid-20th century |

Tertiary Services

communication, energy,

financial, transportation |

Y = f (K, L,

T) |

K = private financial

capital & limited liability corp.

L = organized labour

T = disembodied,

endogenous |

|

Japan

mid- to late 20th

century |

Government

|

Y = f (K, L,

T) G |

K = public & private

capitalization

L = automated labour

T = embodied, exogenous

G = government

coordinates public & private sectors through macro- &

micro-economic policies |

|

Global

late 20th &

early

21st

centuries |

Quaternary

copyright, patent,

registered industrial design, trademark, ‘know-how’,

trade secrets |

Y = f (K, L,

P, O, D) G |

K = knowledge capital

L = knowledge workers

P = physical technology

O = organizational

technology

D = design technology

G = national innovation

system ensures rapid commercial exploitation of

academic or pure research to grow GDP |

Total, Average &

Marginal Product

Assuming that at least one factor of production is fixed (usually

capital), the production curve for total output shows an initially

rising section that peaks and then declines if additional variable

inputs are added (R&L

7-1; M&Y 10th

Fig. 7.1).

No rational producer will go beyond the peak. Why does the curve

peak and then turn down? Congestion. With fixed capital plant and

equipment additional labour initially increases output but

eventually an additional worker simply gets in the way of other

workers and output actually declines.

As additional workers are added each contributes to output. If we

take total output at each level of employment we can calculate both

the average output per worker and the marginal or additional output

contributed by one more worker (M&Y 10th,

Fig. 7.2).

As can be seen, the addition of a worker initially increases the

average output per worker but then the average declines as the

marginal output per additional worker gradually declines following

the Law of Diminishing Marginal Product: the marginal product of

any input will eventually fall as the employment of that input

increases - assuming other factors of production are held constant.

The average product of labour can be calculated as the slope of any

line from the point of origin to the total product curve (M&Y 10th

Fig. 7.4).

Similarly, marginal product can be measured as the slope of the

total product curve (M&Y 10th

Fig. 7.5).

Cost

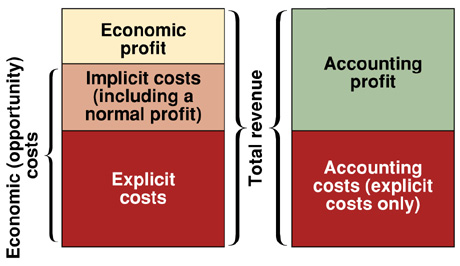

Opportunity Cost

Economic

choice involves how to satisfy infinite human wants, needs and

desires with scarce resources. It requires a choice between

alternatives, e.g., a

pensioner choosing food or medicine. The choice of the best alternative

means the next best alternative is not chosen. Put another way, the

cost of choosing one possibility is the next best alternative foregone.

This is called ‘opportunity cost’. All economic costs are opportunity

costs even those not expressed by market prices.

While

for convenience one usually measures opportunity cost in dollars it

actually involves real alternatives foregone. Thus for a firm,

the opportunity cost of producing (OCP) a good (and therefore opportunity

cost of employing factors of production) is the next best alternative action.

There are two components to a firm’s OCP : explicit and implicit costs.

Explicit costs are paid directly in money; implicit costs or opportunities foregone

are not paid directly in money (even though

measured that way). Explicit costs include direct payment for factors of

production, e.g. in the case of labour,

money cost or wages are generally equal to their OC. Implicit costs include

the implicit cost of physical capital, inventories and the owner’s resources.

(MBB

10th Ed.

Fig. 7.1; P&B not displayed; R&L 13th Ed not displayed)

Fixed, Variable &Total

Assuming one factor of

production is fixed (usually capital) then we are in the short-run

and can identify three types of costs measured in three different

ways.

In the short-run a firm can produce different levels of output but

only by varying variable inputs. Accordingly the firm has three

distinct types of costs:

i - fixed costs associated with the

fixed factor of production - usually K but in the knowledge

industries often L or 'the talent'. Fixed costs must be paid no

matter the level of output, i.e. even if the firm shuts down

fixed costs still have to be paid;

ii - variable costs associated with

variable factors of production - usually L. Variable costs rise and

fall according to how much of the variable factors are employed.

The higher the level of production, all things being equal, the

higher the variable costs; and,

iii - total costs that include all

fixed and variable costs or TC = TFC + TVC (R&L

7-2; M&Y 10th

Fig. 8.6).

Average, Marginal & Total

In turn, for each type of cost at every level of production, average

costs can be calculated:

i - Average Fixed Cost (AFC) = fixed

cost per unit output (M&Y 10th

Fig. 8.7).

AFC will decline as output increases as the fixed cost is spread

over a larger and larger level of output;

ii - Average Variable Cost (AVC) =

variable cost per unit output (M&Y 10th

Fig. 8.8).

The distance between the AVC curve and the TC curve will tend to

narrow as output increases because AFC declines as output increases;

and,

iii - Average Total Cost (ATC) = fixed

(AFC) + variable (AVC) cost per unit output (M&Y 10th

Fig. 8.9).

In turn, for each level of production, marginal cost can be

calculated from the additional cost associated with one additional

unit of output (M&Y 10th

Fig. 8.10).

Average total and marginal cost can also be calculated from the

total cost curve. Average total cost can be derived from the slope

of a straight line or 'ray' drawn from the origin to any point on

the total cost curve (M&Y 10th

Fig. 8.123).

Marginal cost can be derived from the changing slope of the total

cost curve itself (M&Y 10th

Fig. 8.13).

Marginal cost (MC) will initially decline as output increases but

eventually, assuming at least one fixed factor of production, the

Law of Diminishing Returns sets in and marginal cost begins to

rise. The MC curve will cut the average cost curve (AC) at its

lowest point. Thus as long as MC < AC then AC falls; when MC = AC

then AC will be at its minimum; when MC > AC then AC will increase

(R&L

7-2; M&Y10th

Fig. 8.14).

Using the one fixed factor cost function, the long-run cost or

expansion path of a firm is considered to be the sequence of

short-run (SR) scenarios for varying scale of plant and equipment

(M&Y 10th

Fig. 8.15).

In each SR scenario the scale of plant and equipment increases but

during that period plant and equipment are consider to be fixed.

The result is a set of average cost curve for each scale of

production. An envelop curve can then be drawn representing the

long-run (LR) minimum average cost at each level of output (M&Y 10th

Fig. 8.16).

The question remains as to when this series of SR scenarios

becomes the LR.

Supply Curve

The question remains: How much output will a firm be willing to

supply given its cost constraints? Put another way: What is the

firm's supply curve? This depends on how much the firm can get for

its output, i.e. the price or revenue it receives per unit (R&L

9-4; M&Y 10th

Fig. 9.3).

Shut Down

If a firm cannot earn at least enough to cover all of its variable

costs then in the short run it will shut down. This occurs at point

B where marginal cost is equal to minimum average variable cost.

This is called the 'shut down point'. If a firm earns a price

higher than B it can cover all of its variable costs and some of its

fixed costs and it will stay in business. Put another way, the firm

will maximize profits by minimizing losses.

Break-Even

In the long run, however, a firm must cover all costs - fixed and

variable - or it will go out of business. This occurs at point D

where marginal cost is equal to minimum average total cost. This is

called the break-even point. At this point all factors of

production - including entrepreneurship - are fully paid their

opportunity cost. If the firm receives a price higher than the

break-even point then it will earn economic or excess profits. Thus

the supply curve of a firm is the marginal cost curve above minimum

AVC (shut down point) in the short-run and above minimum ATC

(break-even point) in the long-run.

It is important to appreciate that the price or revenue a firm

receives applies to each and every unit of output it sells.

Accordingly it will produce to the point at which the cost of the

next unit of output (MC) equals the price or marginal revenue (MR)

it receives for that last unit. In effect, a firm earns a profit on

each previous unit (if the price or revenue is greater than minimum

AVC or minimum ATC in the short- and long-run, respectively). A

firm thus maximizes profits (or minimizing losses) by producing at

the point where price or marginal revenue equals marginal cost of

the last unit of output.

(17) MR = MC

From the resulting cost

function we can determine

the supply curve of the firm,

(R&L

9-5)

i.e., how much it is willing to produce at each price. The

supply curve is the marginal cost curve of the firm above the

shut-down point in the short-run. If the firm cannot earn enough to

cover all its variable costs, it shuts down. The curve will in the

short-run be upward sloping reflecting the Law of Supply: the higher

the price, the greater the supply; the lower the price the smaller

the supply.

In the long-run, firms can adjust

the size of their plants

(R&L

9-11)creating a series of short-run average and marginal cost curves.

The long-run average cost curve is made up of an envelope of the

minimum points of the short-run average cost curves. In the case of

increasing return to scale industries at some point the most

efficient plant size is achieved where long-run average cost is

lowest. At this point optimal scale is attained and the short-run

marginal cost curve, in effect, becomes the long-run marginal cost

curve.

Elasticity

Elasticity refers to the

sensitivity of one variable to a one percentage change in another.

Price elasticity of supply

refers to the percentage

change in the quantity of a commodity supplied compared to a one

percentage change in its price. The amount supplied can increase:

i) more than

proportionately, i.e. elasticity is greater than one - at the

extreme a horizontal supply curve is perfectly elastic - a small

increase in price results in a large change in the quantity

supplied;

ii) proportionately, i.e.

elasticity is equal to one (unitary elasticity); or,

iii less than

proportionately. i.e. elasticity is less than one (inelastic)

- at the extreme, a vertical supply curve is perfectly inelastic -

any change in price results in no change in the amount of the

commodity demanded or supplied.

Technology

The production function assumes a given level of ‘know-how’, i.e.,

how to transform factors of production into goods. Blithely, we

call a change in such know-how as ‘technological change’. But what

do we mean by technology?

The word ‘technology’ entered the English language only in 1859

deriving from the Greek techne meaning Art and logos

meaning Reason, i.e., reasoned art. It was Karl Marx,

however, (1818-1883) who produced the first true philosophy of

technology combining ‘the means of production’ with a humanist

critique rather than simple glorification of Victorian progress. It

is important to realize that the technological imperative drives

Marxian analysis. Class warfare is collateral damage. This Marxian

connection tainted reception of all subsequent philosophies of

technology especially in the English-speaking world or Anglosphere.

Arguably, it was the work of Martin Heidegger (a purported Nazi)

specifically his 1954 essay ‘The

Question Concerning Technology’ that finally led

in 1983 to founding the American Society for Philosophy and

Technology (Idhe

1991, 4). Please see the journal,

Techne.

Physical technology, to paraphrase Heidegger, is the enframing and

enabling of Nature to serve human purpose. In Economics, however,

technology involves much more than physical technology.

Creative

Destruction & the Solow Residual

In 1942, economist Joseph Alesoph Schumpeter published

Capitalism, Socialism and Democracy. Schumpeter, like Marx,

considered technological change the driving force of capitalism and

human society in general. For Schumpeter

creative destruction is the:

… process of

industrial mutation - if I may use that biological term - … that

incessantly revolutionizes the economic structure from within,

incessantly destroying the old one, incessantly creating a new …

Creative destruction is the essential fact about capitalism. It is

what capitalism consists in and what every capitalist concern has

got to live in. (p.83)

… Every piece

of business strategy acquires its true significance only against the

background of … the perennial gale of creative destruction; it

cannot be understood irrespective of it or, in fact, on the

hypothesis that there is a perennial lull. (pp. 83-84)

From this observation, and other evidence, Schumpeter concluded that

the Standard Model of Market Economics missed the point.

Competition was not about long run lowest average cost per unit

output but rather about innovation and surviving the perennial gale

of creative destruction.

In 1962, economist Robert Solow published “Technical Progress,

Capital Formation and Economic Growth” in the American Economic

Review. In it he presented what is known as the Solow

Residual. It begins with a symbolic equation for the production

function: Y = f (K, L, T) which reads: national income (Y) is

some function (f) of capital (K), labour (L) and

technological change (T).

Technological change in the Standard Model of Market Economics

refers to the impact of new knowledge on the production function of

a firm or nation. The content and source of that knowledge is not a

theoretical concern; what matters is its mathematical impact on the

production function.

Over the last hundred years, depending on the study, something like

25% of growth in national income is measurably attributable to

changes in the quantity and quality of capital and labour while 75%

is the residual Solow attributed to technological change. Yet we

have no idea of why some things are invented and others not; and,

why some things are successfully innovated and brought to market and

other are not. The Solow Residual is known in the profession as

‘the measure of our economic ignorance’. It is why I became an

economist. In what follows I consider the manifold economic meaning

of technology.

The effects of technological change in the orthodox model can be

broken out into two dichotomous but complimentary categories:

disembodied & embodied and endogenous & exogenous technological

change. And at the very edge of orthodoxy are two neologisms not

yet integrated into the disciplinary lexicon: enabling and

disruptive technological change. I will examine each in turn.

Disembodied/Embodied Endogenous/Exogenous Disruptive/Enabling

Implicitly disembodied technological change dominated economic

thought since the beginning of the discipline. It refers to

generalized improvements in methods and processes as well as

enhancement of systemic or facilitating factors such as

communications, energy, information and transportation networks.

Such change is disembodied in that it is assumed to spread out

evenly across all existing plant and equipment in all industries and

all sectors of the economy. It is what Victorians would have called

‘Progress’.

Also implicitly, the concept of embodied technological change traces

back to Adam Smith’s treatment of invention as the result of the

division and specialization of labour (1776). It refers to new

knowledge as a primary ingredient in new or improved capital goods.

The concept was refined and extended by Marx and Engels (1848) in

the 19th and by Joseph Schumpeter in the 20th century with his

concept of creative destruction (1942). No attempt was made,

however, to measure it until the 1950s (Kaldor 1957; Johansen

1959). And it was not until 1962 that Solow introduced the term

‘embodied technological change’ into the economic lexicon, and by

default, disembodied change was recognized (Solow May1962).

Formalization of embodied technological change arguably emerged out

of ‘scientific’ research and development (R&D) during the Second

World War followed by the post-war spread of organized industrial

R&D. This demonstrated that new scientific knowledge could be

embodied in specific products and processes, e.g., the

transistor in the transistor radio. Conceptual development of

embodied technological change has, however, “lost its momentum” (Romer

1996, 204). Many theorists, according to Romer, have returned to

disembodied technological change as the force locomotif of

the economy meaning: “Technological change causes economic growth” (Romer

1996, 204).

While embodied/disembodied refers to form, endogenous and exogenous

refers to the source of technological change. The source of

exogenous technological change is outside the economic process. New

knowledge emerges, for example, in response to the curiosity of

inventors and pursuit of ‘knowledge-for-knowledge-sake’. Exogenous

change, with respect to a firm or nation, falls from heaven like

manna (Scherer 1971, 347).

By contrast, endogenous technological change emerges from the

economic process itself - in response to profit and loss. For Marx

and Engel, all technological change, including that emanating from

the natural sciences, is endogenous. Purity of purpose such as

‘knowledge-for-knowledge-sake’, like religion, was so much opium for

the masses cloaking the inexorable teleological forces of capitalist

economic development. The term itself, however, was not introduced

until 1966 (Lucas 1966) as was the related term ‘endogenous

technical change’ (Shell 1966).

Endogenous change is evidenced by formal industrial research and

development or R&D programs. It therefore includes what are usually

minor modifications and improvements – tinkering - to existing

capital plant and products called ‘development’ (Rosenberg &

Steinmueller 1988, 230). In this way industry continues the late

medieval craft tradition of experimentation. R&D varies

significantly between firms and industries. At one extreme, a

change may be significant for an individual firm but trivial to the

economy as a whole. On the other hand, ‘enabling technologies’ such

as computers or biotechnology may radically transform both the

growth path and the potential of an entire economy. How to sum up

the impact on the economy of the endogenous activities of individual

firms remains, however, problematic.

With respect to the Nation-State, endogenous and exogenous

technological change has a different meaning. They refer to whether

the source is internal, i.e., produced by domestic private or

public enterprise, or external to the nation, i.e.,

originating with foreign sources.

In Economics, two additional terms are slowly entering the lexicon

migrating from business and technology literatures:

disruptive/enabling technologies. The term disruptive technology

was, according to Adner & Zemsky (2005), introduced by Christensen

in 1997. In turn, the Adner & Zemsky article was the first and only

one to include the term ‘disruptive technology’ in its title

according to a JSTOR search of 173 economic journals published

between the 1880s and 2008. A disruptive technology is one that

disrupts existing markets displacing earlier technologies, e.g.,

the automobile displacing the horse and buggy.

On the other hand, the term ‘enabling technology’ has, according to

a similar JSTOR search, not yet been the titled subject of any

economics article. An enabling technology is one that dramatically

increases the capabilities of consumers and/or producers. They are

often characterized by rapid development of derivative or

complimentary technologies, e.g., the IPod and complimentary

goods such as docking stations. Another example is convergence of

telecommunication, the internet and software permitting creation of

JSTOR that dramatically enhances the capabilities of scholarly

researchers.

It is important to note that a new technology may be both disruptive

and enabling at the same time. The internet or worldwide web is an

example. On the one hand it has enabled creation of ‘social media’

such a Facebook; on the other hand, it has been extremely disruptive

of pre-existing business models in the entertainment industry.

Similarly an emerging enabling technology, 3D printing, threatens to

upset traditional mass production manufacturing by enabling small

firms to produce cost-efficient small runs.

Economies of Scale &

Scope

Economies of scale exist when

the cost per unit output falls as output rises. Economies

of scale are due to specialization and division of labour. A firm

will tend to internalize an economic activity if its scale of

production allows it to enjoy such economies of scale.

On the other hand,

diseconomies of scale occur when the cost per unit output increases

as output rises. Diseconomies of scale can occur as a firm grows in

size and complexity. Some things are more cheaply done at a

smaller scale of production, e.g. due to congestion. In fact, some

entire industries are based on 'small scale', e.g. creative products

like art, advertising and R&D. These activities are often more

efficiently conducted in small rather than large firms. In

entertainment and advertising the same result can sometimes be

achieved by creating special small scale production units while the

main administration of the enterprise handles marketing and other

activities that benefits from economies of scale.

Economies of scope are similar to economies of scale but where

economies of scale refers to reductions in the average cost per unit

associated with increasing the scale of a single product type,

economies of scope refers to lowering the average cost for a firm in

producing two or more products. Economies of scale are not

considered in the basic model present here.

External Economies

To this point it has been

assumed that cost is a function only of firm output but cost may

depend upon the output of all firms in the industry. For example,

if industry output goes up, input costs to the firm may go down,

i.e. an external economy to the firm’s production. Or, if industry

quantity goes up, factor costs to the firm may increase, i.e., an

external diseconomy to an individual firm’s production. There are

also what can be called enabling or transformative innovations

outside the economy self in the form of scientific breakthroughs or

within the economy through the spreading of new techniques such as

'just-in-time' inventory systems or communications innovations such

as the internet or QR Codes. Furthermore, such external effects may

be ambiguous, that is they may increase the cost of some and

decrease the cost to other firms. There are also the external

economies available to firms due to location as in industrial

districts or so-called 'clusters' such as Silicon Valley.

Knowledge Domains &

Practices

Domains

Epistemology is the study of knowledge which, for my purposes,

emerges from three distinct knowledge domains. Elsewhere I provide

significantly more detail (Chartrand

2006,

2012). In summary, however,

the Natural & Engineering Sciences generate physical technology,

i.e., the ability to enframe and enable Nature to serve human

purpose. The Humanities & Social Sciences generate organizational

technology, i.e., the ability to shape and mold human

personalities, communities, enterprises, institutions and

societies. The Arts generate design technology, i.e., the

ability to make the best looking thing that works. In effect the

Arts provide the technology of the heart.

Practices

If Domains are concerned with the growth of

knowledge then the Practices are concerned with its application in

satisfying very specific and pressing human wants, needs and

desires. For my purposes, a practice is the “carrying on or

exercise of a profession …, esp. of law, surgery, or medicine; the

professional work or business of a lawyer or medical man” (OED,

practice, 5). I extend this definition to include other

traditional and contemporary professions such as accountant,

architect and engineer.

In turn, a profession is a “vocation in which a

professed knowledge of some department of learning or science is

used in its application to the affairs of others” (OED,

profession, III 6). Put another way, practices “link bodies of

knowledge to forms of action” (Layton 1988, 92). I will, however,

narrow this definition to exclude the now obsolete definition of

profession as “the function or office of a professor in a university

or college; … public teaching by a professor” (OED, profession, IV

7).

Application of professed knowledge to satisfy the

needs of others involves knowledge in action that accounts for

theory, the client/patient relationship and ethics, i.e.,

“the science of morals; the department of study concerned with the

principles of human duty” (OED, ethics, II 2). Professional

ethics, of course, are a socially conditioned and historically

relative.

This distinct form of knowledge may be called

‘praxis’, a term with a colourful history of its own. It was coined

by the alchemist, metaphysician and subsequent saint, Albert Magnus,

about 1255 C.E. He derived it from a Greek noun of action meaning

“doing, acting, action, practice” (OED, praxis,

Epistemology). It was re-coined by Cieszkowski in 1838 to mean

“the willed action by which a theory or philosophy… becomes a social

actuality.” It was then adopted by Marx in 1844 for whom it

explained “how knowledge could give power” not through thought like

Hegel but through the will. In this sense, praxis approximates

design in its emphasis on intent (OED, praxis, 1 c). It also

reflects knowing by doing, not just by the senses or mind. Practice

as experience is another facet of praxis as knowledge. More

generally, praxis means the “practice or exercise of a technical

subject or art, as distinct from the theory of it” (OED, praxis,

1a). For my purposes it will mean ‘knowledge in action’. In this

regard, it is important to remember that knowledge can be used as a

verb as well as a noun (OED, knowledge, v)

The Practices centre on the self-regulating

professions such as accounting, architecture, dentistry, engineering

(applied), law and medicine. Practices engage knowledge in real

life situations while Domains involve knowledge creation or

interpretation, e.g., knowledge-for-knowledge-sake or

art-for-art’s-sake. Praxis is not academic speculation. It is not

knowledge as a noun but as a verb affecting the lives of real

people. As in aesthetics and science, however, the Practices

observe a professional distance from their subject but it is the

very subjective human being. And unlike the atoms, cells and the

physical structures of the NES, people can and do sue for

‘malpractice’. In fact, malpractice and product liability lawsuits

are a hot button political issue in the United States due to their

alleged negative effect on American competitiveness.

The Practices draw, merge, mingle and apply

knowledge and methodologies beyond those internal to their

experience from all three Domains in varying combinations, e.g.,

the use of actors by medical schools to prepare future physicians to

face the emotional realities of patients. Another example is the

Art of Dentistry. Unlike academic disciplines, e.g.,

economics, final certification or ‘licensing’ is not granted by the

university but rather by an independent professional society, e.g.,

a College of Physicians and Surgeons. This partially reflects the

fact that praxis cannot be fully codified, i.e., written

down. Put another way, there is a gap between graduation and

professionalism that must be filled before being licensed to

practice independently. This gap is reflected in the requirement,

in all Practices, of some kind of compulsory apprenticeship,

articling or internship.

In many ways, the Practices are descendents of

medieval guild mysteries operating in the Mechanical Arts. More so

than academic disciplines, the Practices control entry and exit, set

rates, supervise initiates and regulate practice. In the case of

medicine and law they were also the first practical subjects to be

admitted to the university. Some Practices are also associated with

grant-giving or funding agencies such as the Canadian Institutes for

Health Research (formerly the Medical Research Council of Canada)

and the National Institutes of Health in the United States.

Guilds originally received their charters from

the Crown granting them monopoly rights in return for fealty and

sometimes tribute. Today the Practices are regulated by the State,

but as with business law (Commons

1924), most traditional customs and privileges of the

Practices are effectively enshrined, preserved and protected by

legislation under Common Law.

As private institutions serving the public

purpose – including health, education and welfare as well as wealth

and legal rights – the Practices have seldom been acknowledged as

critical players in the competitiveness of nations in a global

knowledge-based economy. How they should be regulated and held

accountable is, however, an important question for public policy in

general and for development of an effective national innovation

system in particular. As demonstrated by Birkenshaw, Harden and

Lewis (1990) in their review of

Government by Moonlight: The

Hybrid Parts of the State in the U.K., USA, France, Germany and

Austria, there are different ways in which this may be done.

More will be said below.

Why

the Firm and not the Market?

The firm is an

institution that hires factors of production to produce goods and

services. Markets are also institutions that can coordinate economic

decisions. Why should some economic activities take place in the one

or the other? The answer is 'cost'. Firms internalize economic

activity because of a number of factors including: transaction

costs, economies or diseconomies of scale and economies of team

production (specialization).

Economies & Diseconomies of Scale

Economies of scale exist when the

cost per unit output falls as output rises.

Economies of scale are due to specialization and division of

labour. A firm will tend to internalize an economic activity if its scale

of production allows it to enjoy such economies of scale.

On the other hand, diseconomies of scale occur

when

the cost per unit output increases as output rises. Diseconomies of scale

can occur as

a firm grows in size and complexity. Some things are more cheaply

done at a smaller scale of production, e.g. due to congestion. In

fact, some entire industries are based on 'small scale', e.g. creative products like art,

advertising and R&D. These activities are often more efficiently conducted in small rather than

large firms. In entertainment and advertising the same result can

sometimes be achieved by creating special small scale production units while the

main administration of the enterprise handles marketing and other activities

that benefits from economies of scale.

Team Economies

Another factor leading firms to internalize certain activities is

specialization in mutually supportive tasks or team production.

Putting a designer together with an engineer and other specialists

within the firm may be cheaper than trying to buy such services on

the market and then try and coordinate their various outputs.

Transaction Costs & Outsourcing

Transaction cost include: the costs of

finding someone with whom to do business; the costs of reaching

agreement on exchange; and, the costs of ensuring such agreements

are fulfilled.

Markets require that buyers and sellers

find each other, get together and negotiate. They also usually

require lawyers to draw up contracts. Rather than buying a good or

service on a market, firm can reduce such cost by internalizing

their production.

It is important to note, however, that

while at any given point in time may be cheaper to buy on a market

rather than produce within the firm (out-sourcing), at another point

in time cost may change and it becomes cheaper to internalize

production of necessary factors of production.

Symbolic Summary of Supply

(8) Q = g (K, L)

where

K, L & Q are fixed in the

very short-run,

K fixed, L & Q variable in the short-run

K, L & Q all variable in the long-run

(12) C = PKK + PLL

where

K = capital

L = labour

PK = price of

capital

PL = price of

labour

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}