|

MACROECONOMICS + 1.0 Introduction Animal Spirits & Psychic Alchemy |

|

1.1 Animal Spirits & Psychic Alchemy

Elsewhere I have

raised the following questions:

What is wealth? What is a nation? And, accordingly, what is “the wealth of nations”? Through time the meaning of

these terms has changed and continues to change and mutate so that today we

stand at the threshold of what is known as ‘the knowledge-based economy’. How did we get here? What force is propelling us into a

future where science fiction becomes ‘economic’

reality? First, over time our

concept of what constitutes ‘wealth’ or alternatively “property”, has mutated

from physical things and persons to increasingly intangible things and

processes, especially the expectation of profit from business transactions

including those most intangible forms of wealth – intellectual property (please

see: J.R. Commons,

The Legal Foundations of

Capitalism, p. 274).

In this regard it should be

noted that econometrics is the sub-discipline of economics explicitly concerned

with quantitative measurement including that of national income and its causal

agents. Other sub-disciplines play

different roles. For example,

institutional and cultural economics are primarily concerned with the

‘qualitative’ nature of such agents as well as their emergent outcome - national

income. In reality, one can not

measure what one cannot name. The

history of national income as well as business accounting is rife with examples

of ‘new’ or ‘creative’ entries being ‘discovered’ then added to the asset and

liability statements of the balance sheet, e.g. ‘goodwill’ as well as new items

to the revenue and expenditure statements, e.g. intellectual property

royalties. Second, over time our

concept of the source of wealth has

mutated and

changed time.

Collectively called ‘factors of production’, these are the causal agents

of, what

Adam Smith

in 1776 called, “the wealth of nations”, or what today is called “national

income” that results from the actions of relatively tangible agents such as

capital, labor and natural resources as well as more intangibles ones including

entrepreneurship and technological change.

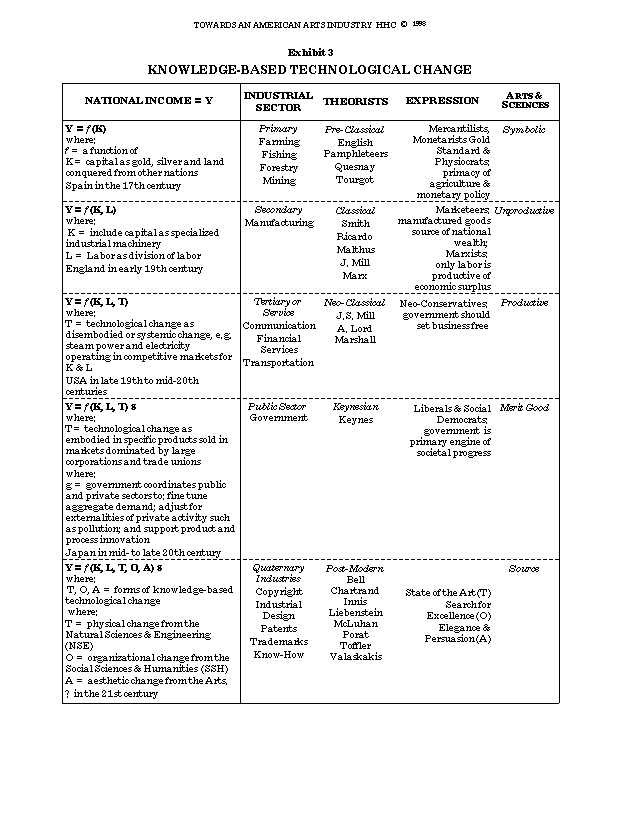

Thus until the late

18th century, national wealth increased, it was thought by the

Mercantilist School of economics, by acquiring more and more ‘capital’ in

the form of gold, silver and land (including chattel [‘moveable property’] which

comes from the Anglo-Saxon word for ‘cattle’) as well as more slaves, serfs,

peons, habitant and other human beings effectively ‘owned’ by a nation. By the mid-19th century the

concept expanded with the Classical School to include manufacturing plant and equipment combined

with division and specialization of labor.

By the last quarter of 19th century, it grew further with the Neoclassical School to embrace large-scale financial capital (especially

limited liability equity markets), increasingly organized labor and

‘disembodied’ technological change referring to general or systemic ‘progress’

in fields like transportation, manufacturing and communications. With the Keynesian School of the mid-20th century it expanded to

encompass the role of government in managing the wealth of nations as well as

‘embodied’ technological change referring to the specific marketable results of

organized research and development in the natural and engineering sciences, e.g.

the transistor in the transistor radio.

Today our conception increasingly focuses on intellectual property

including formal rights such as copyrights, patents, registered industrial

designs and trademarks as well as informal rights including ‘know-how’ and trade

secrets constituting what I call ‘the quaternary sector’ of the economy

complementing the three standard sectors: primary (agriculture, farming, fishing

and forestry); secondary (manufacturing); and tertiary (services). And with this development we have

entered the ‘knowledge-based economy’.

It is important to note that this economic evolution has been paralleled,

if not propeled, by legal evolution defining ever more intangible forms of

property rights (please see J.R. Commons,

The Legal Foundations of

Capitalism). The success of this new

economy depends particularly on two factors of production and their interaction

– entrepreneurship and technological change. Entrepreneurship is, compared to fixed

plant and equipment, workers and raw materials, a very ill-defined, intangible

factor of production. The word

‘entrepreneur’ comes from the French entreprendre which can be translated

alternatively as: (a) “undertaking” as the person in effective control of a

commercial undertaking; or, (b) “middling” as a contractor acting as an

intermediary. Undertaking

responsibility for a commercial venture or middling between producers and

consumers involves risk. The

willingness to undertake such risks are what John Maynard Keynes (p. 161) called the “animal spirits”. Since the time of John D.

Rockefeller Senior and the “Robber Barons” the business tycoon, the man (and

increasingly the woman) whose vision is ultimately realized in economic space,

has been an icon of both ‘democratic’ and economic thinking. Today the entrepreneur formerly

known as “Bill Gates” bestrides the globe opening and closing windows unto the

future. Thirty years ago he was a

‘nobody’, today this sometimes “richest man” in the world wrestles with his

co-patriot, Sam Robson Walton founder of Wal-Mart, for the title. But it is no longer just ‘captains of

industry’ who are ‘risk-takers’ for we have become an entrepreneurial society in

which a near majority risk financial capital, indirectly through RRSPs, company

retirement and ‘stock option’ plans (whose value is based on the market value of

a company’s stock) and mutual funds, or directly through equity ownership bought

and sold on the stock market.

The waxing and waning of

the animal spirits of investors and entrepreneurs, measured by investment in

real and financial capital, is a major cause of the so-called business cycle. The recent

‘dot.com bubble’ is an example of the impact of animal spirits, the

sense of risk-taking, that fuels the capitalist economy. Thus behind all of the equations and

‘rational’ economic models lays sheathing passion, greed and fear summed up in

Keynes’ term ‘animal spirits’. Keynes’s whole theory of

unemployment is ultimately the simple statement that rational expectation being

unattainable, we substitute for it first one and then another kind of irrational

expectation: and the shift from one arbitrary basis to another gives us from

time to time a moment of truth, when our artificial confidence is for the time

being dissolved, and we, as business men are afraid to invest, and so fail to

provide enough demand to match our society’s desire to produce. Keynes in the General Theory attempted a

rational theory of a field of conduct which by the nature of its terms could be

only semi-rational. Shackle,

p. 129 The other key factor is

technological change or what Joseph Schumpeter called ‘creative destruction’. The

contribution of technological change to growth in national income has been

estimated as high 66% (Shapiro,

p. 493). However,

we have no idea of why

somethings are invented while others are not, and why somethings invented are

innovated (brought to market) and others are not. In this

sense, the contribution of technological change to national income can be called

the ‘measure of our economic ignorance’.

It is important to note the two stages nature of this ignorance –

invention and innovation. While

invention appears to be a matter of realizing a natural science potential,

innovation is a matter of social or cultural factors. For example, the electric battery was

apparently invented more than 2,000 years ago outside what is now

Did Bill Gates or Sam

Robson Walton graduate from an ivy league “B” school? In fact, historically the most

successful economic alchemists have been mainly ‘outsiders’. Thus the founders of the Industrial

Revolution were ‘dissenters’, i.e., not members of the Church of England, and

excluded from the university. Eventually they became part of the establishment

with the result being what in economics was called in the last quarter of the

20th century, “the British disease” (please see:

English Culture and the Decline of the Industrial Spirit,

1850-1980 by Martin J. Wiener). The place

of … intellectual property is, after all, the

only absolute possession in the world...

The man who brings out of nothingness some child of his thought has

rights therein which cannot belong to any other sort of property… (Chaffe

1945). As a student I was told

that: “An economist is a tool bearing animal but the tool box is in his

head”. And what are the tools? Concepts! In this regard the word ‘concept’

derives from the Latin capere “to

take”, and was originally used in

the sense ‘to grasp firmly with the hand” or in Sicilian, “to steal”. So let’s take an inventory of what tools

you should be carrying, given the prerequisites for this

course. From your introductory and

intermediary microeconomics courses you should have a working knowledge of:

elasticity, equilibrium, externalities, marginal and opportunity cost, supply

(producer theory), demand (consumer theory) and markets (competition

theory). From introductory

macroeconomics you should know something about aggregate demand and supply,

comparative advantage, expectations, marginal propensity, money and the multiplier – all in

the Keynesian tradition. To this point these are

just a loose collection of tools you have ‘learned’ about. In this course they will be put to work;

some new ones will be added; and skill in using them assessed. Some of you will take them further,

refining and polishing their use, even creating new ones, through a career in

economics; but for all, however, you should come away with a sound grounding in,

and understanding of, the major economic theories guiding a post-modern world

striving for higher and higher levels of national income, and, hopefully,

higher and more equitably distributed global income together with a better, more fulfilling way of life for all

citizens of planet Earth. We will take these tools

and use them to construct and then operate the three primary engines of

macroeconomic analysis – Classical, Keynesian and Monetarist. We will then tinker with these

‘standard’ engines to construct mixed or hybrid engines. We will then ‘road test’ them on the

fiscal, monetary and growth policy highway system of national macroeconomic

policy. However, not only will

these engines be tested, your driving ability will also be assessed and

rated. To help you along the way

the website provides some pit stops that may prove helpful. The

Glossary

of the text is provided on-line.

Various ‘in-depth’

articles and extracts are provided so you more easily immerse yourself in

economic thinking and gain a somewhat different perspective from that presented

in the text book. Finally all my

lecture notes will be available on-line and will include links to relevant

graphics and other teaching aids.

|

{kind=link}